Goals-based investing, a revolutionary approach to wealth management, takes center stage in Tony Davidow’s groundbreaking book. This visionary framework challenges traditional investment strategies, offering a fresh perspective on achieving financial objectives. Davidow’s insights promise to reshape how you view and manage your portfolio.

Dive into this review to unlock the secrets of goals-based investing and discover how it can revolutionize your financial future.

Table of Contents

- Genres

- Review

- Introduction: Learn why goals-based investing is the future of the financial-services industry.

- The financial services industry is in a state of continuous evolution.

- Goals-based investing is an antidote to the limitations of modern portfolio theory.

- Advisors and investors need to be aware of their cognitive biases and how these may affect their investment decisions.

- Even after the rise of passive investment, active management has its place.

- Alternative investments and sustainable investing are becoming attractive options.

- Goals-based investing requires an analysis of what you want to achieve through investment.

- Successful wealth advisors must navigate and adapt to the changes coming over the next ten years.

- About the author

- Table of Contents

Genres

Finance, Wealth Management, Personal Finance, Economics, Business Strategy, Financial Planning, Portfolio Management, Retirement Planning, Behavioral Economics, Money and Investments, Derivatives Investments, Bonds Investing, Private Equity, Analysis, Strategy

![[Book Summary] Goals-based Investing - A Visionary Framework for Wealth Management](https://lh3.googleusercontent.com/pw/AM-JKLU08-oKdF2BeBAfRtKz-mRDuyG4b-eBRYAmb4Tl2JVkP6XqTzZOJ6WMsvDg0dRyXjzfUDoKq_UrwzQAmyNv8dOL0V6fJDWkm86HWKfuT2PiylM1IEQqxe--6du2z6k5y1V2Yu6KxiKTUjRwcbwVJKwdjw=w548-h820-no?authuser=0)

“Goals-based Investing” introduces a paradigm shift in wealth management. Davidow argues that traditional approaches often fall short in meeting investors’ specific needs. Instead, he proposes a framework that aligns investment strategies with individual goals.

The book delves into the psychology of investing, exploring how emotions and biases impact financial decisions. Davidow emphasizes the importance of understanding each client’s unique circumstances, risk tolerance, and long-term objectives.

He outlines a step-by-step process for implementing goals-based investing:

- Identifying and prioritizing financial goals

- Assessing risk tolerance and time horizons

- Developing customized investment strategies

- Constructing portfolios tailored to specific objectives

- Monitoring progress and adjusting as needed

Davidow provides case studies and practical examples to illustrate the application of his framework. He discusses how goals-based investing can be particularly effective for retirement planning, education funding, and legacy creation.

The book also addresses the role of technology in implementing goals-based strategies, exploring how AI and data analytics can enhance the investment process.

Review

Davidow’s “Goals-based Investing” offers a refreshing take on wealth management. Its strength lies in its client-centric approach, which resonates in today’s personalized world.

The book’s structure is logical and easy to follow. Davidow’s writing style is clear and engaging, making complex concepts accessible to both finance professionals and individual investors.

One of the book’s standout features is its practical orientation. The inclusion of real-world examples and case studies helps readers understand how to apply the concepts in their own financial planning.

However, some readers might find certain sections repetitive. Additionally, while the book provides a solid foundation, it could benefit from more in-depth discussions on implementing goals-based strategies in various market conditions.

Davidow’s emphasis on behavioral finance adds depth to the discussion, highlighting the often-overlooked psychological aspects of investing.

The book’s forward-looking perspective on technology in wealth management is particularly valuable, offering insights into the future of the industry.

Overall, “Goals-based Investing” is a valuable resource for financial advisors, wealth managers, and individual investors seeking a more personalized approach to portfolio management. It challenges conventional wisdom and provides a framework that could potentially lead to more satisfying investment outcomes.

Introduction: Learn why goals-based investing is the future of the financial-services industry.

Goals-Based Investing (2022) explains how the wealth management industry is transforming, how modern portfolio theory is no longer considered modern, and how product evolution and regulatory changes are making it easier for investors and advisors to access market segments that were once the exclusive domain of large institutes.

The financial-services industry has been changing over the last decades to serve investors better. Failure by financial advisors to understand and adapt their approach to these changes will ultimately have an impact on their success.

So let’s take a whistle-stop tour of how the industry has been changing, discuss why modern portfolio theory and its successors are flawed, examine active and passive management, define what alternative investment actually means, present goals-based investment as a way to meet the objectives of high-net-worth families, and look at some predictions for the industry’s future. That’s a lot to get through, so let’s get started.

Keep in mind that this is not financial advice. Rather, it’s an analysis of the past, present, and possible future of the wealth-management industry, and how you can be better prepared for it.

In this summary, you’ll learn

- why there is a place for both passive and active investment management;

- about the role of alternative investment strategies; and

- how to establish a goals-based investment portfolio.

The financial services industry is in a state of continuous evolution.

Whether you’re a seasoned investor or relatively new to the topic, you might not know exactly who the key players in the financial-services industry are, and how their roles in wealth management differ. So, let’s start with a quick overview.

First, there are wealth-management firms. These include companies like Morgan Stanley and Merrill Lynch. Such companies carry out research and due diligence. They also provide support to financial advisors. The financial advisors themselves work for the wealth-management firms, advise clients directly, and may also use asset managers to provide investment advice. Then there are custodians. Examples include companies like Schwab and Fidelity. They provide custodial services, technology, research, and trading support. And finally, we have asset managers such as Blackrock, Fidelity, and JP Morgan. These companies manage money via mutual funds, exchange-traded funds (ETFs), hedge funds, and other structures.

Some of these companies also provide multiple services. For example, Morgan Stanley has retail and private-wealth divisions, but also has asset-management subsidiaries.

Over the last 20 years, the financial sector has changed considerably – and so has the relationship between the various companies within it. It’s also likely that it will change further over the coming decade.

Back in 1975, the founder of The Vanguard Group, Jack Bogle, created the first index fund. He was skeptical about the need for financial advisors and believed that investors could do just as well left to their own devices. Vanguard is now the second-largest asset manager worldwide with over $6 trillion in assets under management. After the general financial crisis, growth in do-it-yourself investment grew rapidly as investors began to question why they should use investment managers if they couldn’t protect them from market collapses. The use of ETFs accelerated after the crisis and advisors also began to use them more in building portfolios.

And then came COVID-19, the pandemic that stopped the world. It ushered in not only health issues but financial woes. The markets became very volatile and uncertainty reigned. Investors, shocked by rising death tolls, also watched helplessly as their wealth plummeted.

Over the years, wealth-management practices have also needed to reinvent themselves in order to provide new services to their clients. This has required reskilling and training in order for advisors to understand issues such as estates, tax management, lending options, and charitable giving, for example.

Financial advisors needed to help their clients through these troubled times, and in innovative ways – through the use of technology to reach their clients, for example. In a post-pandemic world, it is still unclear how financial advisors will engage with clients in the future. What is clear, though, is that they need to rise to the challenges that the sector faces now and in the coming decade, evolve their approach, or risk being replaced by robots and AI and ultimately becoming obsolete.

Goals-based investing is an antidote to the limitations of modern portfolio theory.

You might be familiar with the term modern portfolio theory, or MPT. This idea was developed by Nobel Prize–winner Harry Markowitz, who said that “diversification is the only free lunch in investing.” He posited that by combining risky investments which were not in lockstep with each other, greater returns could be achieved with much lower risk.

MPT, though, has its limitations. It assumes that all investors are risk-averse, whereas, in reality, not all investors will select the optimal, less-risky option. In fact, they are often chasing greater returns.

So what are the alternatives, and why is a goals-based approach more appealing?

In 1991, Post-MPT came along. It’s pretty similar to MPT but defines risk differently and also how the risk will influence expected returns. Then, in 1992, the Black-Litterman model arrived. This model is based on the premise that assets perform in the future just as they have in the past – or the equilibrium assumption.

These and other alternatives have drawbacks too. For example, post-MPT suffers from accuracy of data in the same way as MPT, as future results may not correspond with historical data. And the Black-Litterman model uses projections of future results, which actually may also be flawed.

The financial world has changed a lot since Markowitz published his paper, but Goals-based investing shifts the goalposts. Rather than concentrating on beating the market, maximizing returns, and minimizing risks, it concentrates on progress toward the investor’s goals and reinforces the idea of long-term investing. It balances risk and returns and seeks to achieve desired outcomes – whether that’s for capital appreciation, wealth preservation, savings for a second home, college funding, charitable donation, or retirement income.

Next, we’ll examine the roles of passive and active investment management and alternative investments – in particular, hedge funds and innovations in private markets – and then we’ll consider the rise of sustainable investing, before returning to discuss goals-based investing a little further on.

Advisors and investors need to be aware of their cognitive biases and how these may affect their investment decisions.

Investors don’t always act rationally. But why is that?

In a nutshell: cognitive biases. Many investors will do whatever it takes to avoid financial loss – a cognitive bias known as loss aversion. Or they may begin to believe that they’re capable of picking stocks or managers who will outperform the market – aka illusion of control bias. Then there’s recency bias, which makes one believe that strong results in the present can be extrapolated into the future. And herd mentality, where investors may pursue stocks because they’re suffering from FOMO – the fear of missing out.

So if investors suffer from all of these biases, what can the poor financial advisor do? Well, first and foremost they need to recognize that they themselves suffer from the same biases. Then, they need to remind clients of their goals and objectives, and advise them against acting on emotions and impulse. Here, it can help to have an investment policy statement that allows advisors to take action without permission and to do “the right thing” on behalf of their clients.

As an advisor, you should also be conscious of how you frame each discussion. Use simple language. Avoid jargon and confusing terminology. Try using an analogy or story when explaining complex topics. Clients will respond more positively if you give clear explanations.

Davidow uses an analogy when explaining asset allocation to clients: building a portfolio is like making an omelet. A good omelet requires the right ingredients in the right quantities. It includes eggs, cheese, onions, and then maybe mushrooms, sausage, or other tasty extras. Each ingredient, Davidow explains, is like an asset class. But not everyone will follow the same recipe. Some investors might exclude emerging markets from their portfolio – just as some people might exclude onions from their omelet.

Financial advisors are here to teach clients about financial markets and asset allocation. But if you want to increase your credibility and earn more respect, you should also teach them about behavioral finance. Clients need to know that they’re not alone in reacting to their emotions and that it’s not always easy to overcome irrational impulses.

Even after the rise of passive investment, active management has its place.

In 1973, in his book A Random Walk Down Wall Street, Burton Malkiel made a bold statement: “a blindfolded monkey throwing darts at a newspaper’s financial pages could select a portfolio that would do just as well as one carefully selected by experts.” His book began the debate about active and passive investment management and effectively kick-started the passive-investing revolution. Vanguard introduced the first index fund in 1975; later, in 1993, State Street Global Advisors launched the first exchange-traded fund, or ETF.

ETFs made it easy for investors to access the market cost effectively and tax efficiently. It meant that they could access the S&P 500 – that’s the Standard and Poor’s 500, a stock market index which tracks the performance of 500 companies on the US stock exchange – in a single trade without transaction costs and with built-in automatic rebalancing. Prior to this, it was a costly process and an investor’s exposure would inevitably deviate from the index over time.

There are now over 2,200 ETFs available in the US. They amount to some $6 trillion in assets under management. ETFs started out as cheap, efficient passive investing options. They both mimicked the market and provided affordable access to the market. Now they represent a range of smart options that use alternative weighting strategies, including factors such as value, size, quantity, volatility, and momentum. In other words, ETFs now offer advisors even greater flexibility when building portfolios for their clients.

But the rise in passive investment doesn’t mean there isn’t room for active management. Indeed, many successful fixed-income ETFs are actively managed, and there’s an active element to each. So the question really shouldn’t be whether active or passive investing is better but how active and passive strategies can be best used.

And large wealth-management firms are currently developing new asset-allocation models – models that use ETFs, mutual funds, and separately managed accounts (SMAs) as “building blocks.” These models provide benefits to both advisors and investors by aligning the interests of the advisors with those of their clients. Advisors get more expertise from asset managers, and investors get access to specialized teams of experts.

In spite of the new models, there’s always going to be a need for customization of portfolios to suit the specific requirements of some high-net-worth and ultra-high-net-worth families. This includes the use of so-called alternative investments, which we’ll explore next. The good news is that the industry now has a wide range of tools at its disposal to build appropriate portfolios to fully meet most clients’ needs.

Alternative investments and sustainable investing are becoming attractive options.

The term alternative investments often creates fear and confusion in investors. So let’s start by clearing up what the term actually means. Put simply, alternative investments means hedge funds and private markets – that’s private equity, private credit, and real assets. Hedge funds, though, aren’t available to everyone – only qualified purchasers and accredited investors. To be accredited, you need to have a net worth over $1 million or an annual income over $200,000. To be a qualified purchaser, you need at least $5 million in investments.

So why should we consider alternative investments in a portfolio? Well, there are three main factors to think about.

First, there’s the market environment. The next decade will be characterized by lower traditional equity returns and bond yields. The market will have to deal with the impact of the COVID-19 pandemic, assets with negative yields, rising inflation, and growing tension around the world. Alternative investments may help to dampen volatility, provide alternative sources of income, and perhaps even provide better returns.

Second, innovation in products has allowed managers to offer investors alternative strategies where previously access wasn’t possible due to requirements for accreditation and minimum investment values.

And third, it’s easier for privately offered funds to market themselves as a result of regulatory changes. For example, the Jumpstart Our Business Startups (JOBS) Act allowed crowdfunding to operate and also made it easier for hedge funds and private equity to be marketed directly to investors.

Let’s look more specifically at hedge funds. The first hedge fund was launched in 1949 by Alfred Jones – “the father of the hedge fund” industry. Jones used long and short stocks in equal proportion and his results required the right stocks to be bought and sold. By limiting the number of investors to 99 and using limited partnerships, he avoided the requirements of the Investment Company Act of 1940. Jones took 20 percent of the profit in compensation.

Today’s hedge funds retain many of the characteristics of Jones’s model. A partnership model is still used, and the fund manager is paid a percentage of the profits. The number of partners is limited, and, in the same way, long and short stocks are bought and sold. As part of a portfolio, hedge funds can often provide stronger returns and also protect capital through risk management.

Many investors are unaware that not all hedge funds are the same. For example, there are equity-hedge, event-driven, relative value, macro, and multi-strategy solutions which have their own mechanisms for asset management.

Now let’s turn our attention briefly to the innovations in private markets – private equity, private credit, and real assets. Once the domain only of large institutions, product innovation in recent years has also allowed these investments to become available to more investors.

There’s a whole spectrum of private-equity investment opportunities depending on where a company is in its development. For example, at one end of the spectrum, we have venture capital – an investment in an early-stage company that’s still in the process of developing its product or service. At the other end, there are buyout cash-flow-positive companies that may benefit from restructuring or from the sale of some assets. Private-equity managers can offer value by launching new products and services, spinning off noncore business, or making strategic acquisitions, for example.

Both advisors and investors need to understand the stages of development and the risks involved before investing in private equity. Investors need guidance from wealth advisors to answer such questions as: What role do private markets play in a client portfolio? How can the options be evaluated? And how much investment should I allocate to private markets?

Finally, let’s consider growth in sustainable investing. This has perhaps been the biggest trend across the financial industry, but many investors still believe that they have to give up returns in order to do good in their investment portfolio.

A number of terms are often used interchangeably. Socially responsible investing (SRI). Environmental, social, and governance (ESG). Impact investing. Sustainable investing. But they’re not the same.

Back in the 1990s, SRIs became popular as a way to express views about unpopular activities. If an investor disliked tobacco or alcohol, for example, companies or stocks could be excluded from a portfolio. But this often meant sacrificing returns.

On the other hand, ESG screening, which has become increasingly popular in recent years, assigns a weighting to companies with the best practices. Such strategies often outperform comparable unconstrained indices.

Impact investing concentrates on the allocation of funds to private companies which endeavor to deliver positive social and environmental impacts.

Sustainable investing, which is a broad umbrella that covers SRI, ESG, and impact investing, has grown considerably from $12 trillion in 2018 to $17.1 trillion in 2020. It accounts for nearly one-third of all US professional assets under management. Within this figure, the largest investment comes from public funds, amounting to approximately $3.4 trillion.

As sustainable investing becomes more and more mainstream, wealth advisors need to seize the opportunity it presents. Incorporating sustainable investing into clients’ portfolios may increase the probability of investors achieving their goals, and, in turn, advisors may reap the rewards of bigger dividends in the future.

Goals-based investing requires an analysis of what you want to achieve through investment.

Think for a minute about managing your family budget. Imagine you have a “pot” for your rent, another for the bills, another for the food for the week, a couple of others for other specific purposes, and finally – if anything is left over – one for vacation expenses.

Goals-based investing is pretty similar. Instead of a single investment pool, you separate your investments into different “pots,” each relating to a particular goal you wish to achieve. Your goals might, for example, include generating retirement income, creating a college fund for the kids, charitable giving, wealth accumulation, or other outcomes that fit your requirements. Each of your goals has different cash-flow needs and time horizons, so it makes sense to have multiple portfolios rather than just one.

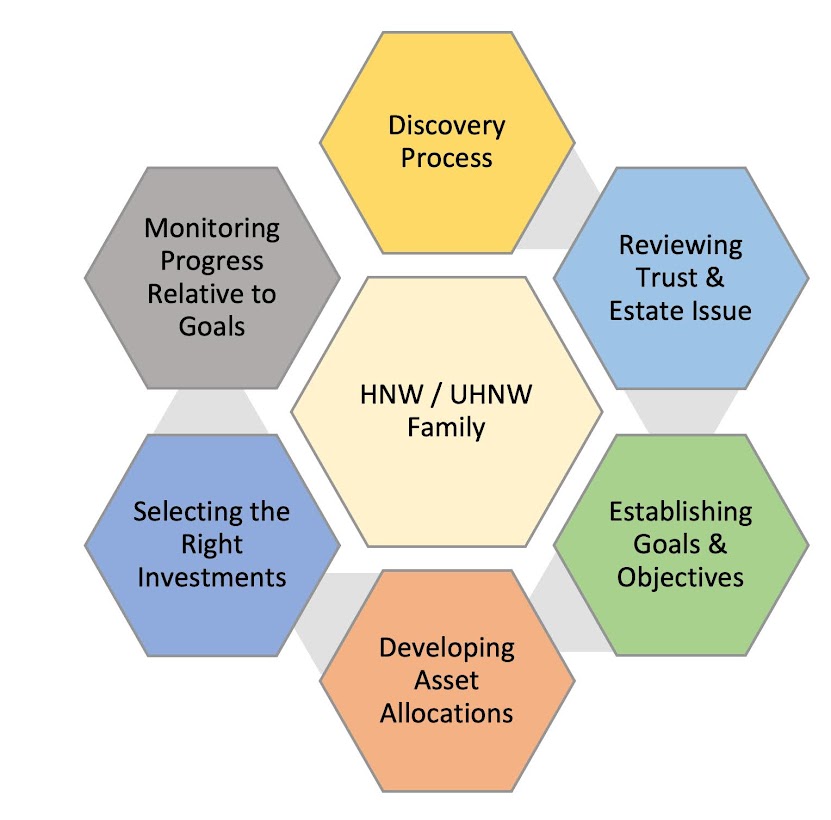

Let’s imagine for a moment that you have a high-net-worth family client that’s interested in a goals-based-investment approach.

The first step in working with your client is one of discovery. It’s important to understand what the family needs and wants. What makes it unique? Then, an analysis of estate and trust issues is required. Does a trust already exist? Multiple trusts? How are assets to be distributed? Third, you need to understand the goals and objectives of the family. What needs are there to be solved? What are the cash-flow requirements and projected time horizons?

The fourth step is to develop asset allocations. Here, as in step three, you need to understand what the return objectives are, income requirements, and time horizons. When you have this information, the fifth step is to select the right investments. You’ll need to look for funds or managers who can provide the required outcomes considering ETFs, SMAs, registered funds, or private funds. How do you want to incorporate active and passive strategies? And do alternative investments play a part in the portfolio?

Finally, you’ll need to monitor progress toward goals. Keep track of how accounts are performing relative to their required objectives. And also be aware of changes in the family’s needs or circumstances in order to make any portfolio changes necessary. It’s important to evaluate the progress toward goals consistently.

Remember that the client’s portfolio may be a way to achieve desired outcomes, but this doesn’t mean you can ignore performance. You still need to adopt the best investment strategies possible. The assets within a portfolio are like pieces of a jigsaw puzzle. If you put the pieces together correctly, they form a clear picture – a picture of what the portfolio is intended to achieve. Put them together haphazardly and, well . . . that picture is less than clear!

When explaining investments to clients it’s useful to organize them into three groups: growth, income, and defense. Growth of the portfolio might come from equity allocation in large, small, international, and emerging markets. Income might come from treasury, corporate, or government bonds. And the inclusion of gold as an investment is to provide security and stability against market shocks – defense.

When engaging with a high-net-worth family, you may want to suggest that they develop a mission statement if they don’t have one already. This helps clarify what the family wishes to achieve and how it will pass on its values from generation to generation.

Over the last ten years, there’s been a rapid change in the market and it seems inevitable that there’ll be further changes over the coming decade. So let’s conclude our whirlwind tour of wealth management and goals-based investing with a look at some predictions for what the next ten years hold for the industry.

Davidow believes that there will be a shift in demographics to younger, more diverse investors. He also predicts that goals-based investing will become the norm. McKinsey & Company shares his view, predicting that at least 80 percent of advisors will be offering goals-based-investment advice by 2030.

Let’s finish up by looking at three ways the industry may change in the next decade.

First, wealth advisors will differentiate themselves from the competition through education, and those with specialized training will be at a premium. Specialist educational organizations will have to provide continually evolving education programs to both advisors and their clients.

Second, commissions will continue to fall and eventually trading will become commission-free. Revenues will come from other sources such as from using affiliated products in model portfolios, revenue-sharing relationships with asset managers, and by lending securities. Of course, savvy investors will understand that commission-free doesn’t actually mean free.

And, third, artificial intelligence will learn more about client needs and behavior, and will help advisors understand which strategies will work best for their clients. AI will probably also help advisors anticipate client needs, improve outcomes, and even strengthen the relationship between advisor and client. But AI will always lack empathy – which is why it will never replace good wealth advisors.

Wealth-management advisors will need to adapt and respond to these changes and to the changing needs of their clients.

Changes are coming – great changes – and the successful wealth advisors will be the ones who can navigate and adapt to these changes by evolving their value proposition and how they serve their clients.

Tony Davidow, CIMA, is president of T. Davidow Consulting, an independent advisory firm focused on the needs and challenges facing the financial services industry. Davidow leverages his diverse experiences to deliver research and analysis to sophisticated advisors, asset managers, and wealthy families. He has held senior leadership roles at Morgan Stanley, Charles Schwab, Guggenheim Investments, and Kidder Peabody among others. He is focused on developing and delivering content relating to advanced asset allocation strategies, alternative investments, factor investing, sustainable investing, and other topics. In 2020, Davidow was recognized by the Investments and Wealth Institute, with the Wealth Management Impact Award, which honors individuals who have contributed exceptional advancements in the field of private wealth management.

Table of Contents

Acknowledgments v

Foreword ix

Introduction xiii

Chapter 1 The State of the Financial Services Industry 1

Chapter 2 The Evolution of Wealth Management 23

Chapter 3 Becoming a Behavioral Coach 49

Chapter 4 Challenging Modern Portfolio Theory 69

Chapter 5 Incorporating Active and Passive Strategies 89

Chapter 6 The Role and Use of Alternative Investments 109

Chapter 7 Innovations in Private Markets 129

Chapter 8 Sustainable Investing 151

Chapter 9 Goals-Based Investing 169

Chapter 10 The Future of Wealth Management 189

Notes 207

Index 211