Consumers are telling us that connected TV (CTV) is part of their daily lives. In fact, for a large majority of American viewers streaming has become the core means of ‘watching TV’ — as 80 percent of TV viewers say they watch either subscription services, ad-supported services, or virtual MVPDs (vMVPDs) weekly or more often.

Additionally, cord-cutting is no longer a trend among the young or tech-savvy, it’s quickly becoming a norm. As a result, advertisers are taking notice, adapting their strategies to include both connected TV and traditional linear TV.

Read this article for more insights, including:

- Younger consumers remain firmly at the leading edge of cord-cutting, as 60 percent of adults 18-34 report they do not subscribe to traditional cable services.

- 92 percent of advertisers view CTV ad performance as on par with — or even more effective than — linear TV.

- 70 percent of advertisers say their top priority for 2021 TV investments is linking video investments to business outcomes.

- 65 percent of U.S. adults 18–34 reportedly turn to streaming to get their sports fix.

Content Summary

Table of Contents

About this article

Introduction

Younger demographics signal TV’s future

Advertisers see CTV as being on par with, or even more effective than, linear TV

Sports become far more accessible through CTV

Connected TV and linear TV move closer together

About this article

This article comprises and summarizes the results of consumer and advertiser surveys regarding TV viewing and advertiser trends.

The Trade Desk conducted an advertiser study with Advertiser Perceptions, surveying 150 advertisers in the United States. There was a 50/50 split between agencies and brand-direct advertisers. The vast majority were director-level and above (81 percent representing directors, VPs, and C-level executives). Fieldwork was conducted between April 22 and May 5, 2021.

For the consumer study, we partnered with YouGov to survey more than 3,800 adults (18+) TV viewers in the U.S. Field work was conducted between April 27 and May 5, 2021. We qualified “TV viewers” as consumers with at least one screen in their household which can be used for viewing TV content.

Introduction

Consumers are telling us that connected TV (CTV) is part of their daily lives. In fact, for a large majority of American viewers streaming has become the core means of ‘watching TV’ — as 80 percent of TV viewers say they view either subscription services, ad-supported services, or virtual MVPDs (vMVPDs) weekly or more often. Additionally, cord-cutting is no longer a trend among the young or tech-savvy, it’s quickly becoming a norm.

Our report reveals that many of the consumption shifts that were accelerated by the pandemic have become cemented. It shows that consumers are adaptable and fluent in the new TV ecosystem, and as a result, they are moving back and forth between different viewing modes and vehicles with ease.

One key example here is the shift of live sports onto streaming apps. Tentpole events like the Super Bowl, or the Olympics, were long considered to be linear mainstays, but that’s no longer the case. New data shows that viewers are increasingly inclined to watch such big events via CTV and that, in turn, opens up new opportunities for advertisers to reach new audiences.

No doubt, advertisers are paying attention to these consumer habits — according to our data with Advertiser Perceptions — and many are beginning to view streaming and CTV as an essential, more measurable element when it comes to ad-buying practices. Furthermore, the proliferation of streaming has shaken up traditional TV processes, such as the annual upfronts, which have necessarily adapted to give marketers more scope and flexibility in both linear and CTV buying practices.

Key Findings

- Cordless viewing grows: Nearly half of U.S. TV viewers (47 percent) are already cordless and of those who still subscribe to cable, 42 percent plan to cut or pull back their package in the next year.

- Younger TV viewers prefer streaming: Younger consumers remain firmly at the leading edge of cord-cutting, as 60 percent of adults 18-34 report they do not subscribe to traditional cable services.

- Cost drives adoption of ad-supported services: Nearly two-thirds of U.S. TV viewers (64 percent) don’t want to spend more than $30 a month on streaming services, making free or lower-cost ad-supported services more attractive to consumers.

- CTV ad performance is seen as on par with — or even more effective than — linear TV: An overwhelming majority of advertisers (92 percent) view CTV as just as effective if not more effective than linear TV.

- Advertisers prioritize ROI: 70 percent of advertisers say their top priority for 2021 TV investments is linking video investments to business outcomes.

- Streaming sports accelerates in TV viewers 18–34: 65 percent of U.S. adults 18–34 reportedly turn to stream to get their sports to fix.

- Uptick in CTV advertising for marquee live events: 74 percent of marketers report buying CTV ads in conjunction with live sporting events can be more cost-effective and impactful than classic sports sponsorships.

Younger demographics signal TV’s future

While cord-cutting has been a growing trend for years, the events of the past year have served to fan the cord-cutting flames. Now that the world is adapting to its new normal, streaming has become a primary way to access TV for many — and this number is likely to grow as Americans appear to be reassessing their relationship with pay-TV bundled services.

Already, nearly half (47 percent) of U.S. TV viewers state they do not subscribe to “traditional cable,” and among those that do, 44 percent are planning to drop cable or cut back on services over the next year. Of the viewers who have already cut the cord, more than half (59 percent) claim that they are unlikely to go back.

Cost, along with the perceived value of the traditional cable bundle, is a major factor. More than half (52 percent) of those who have canceled their cable subscription or plan to do so said that cable subscriptions don’t offer enough value for the money paid, and 43 percent said that they only had an interest in a handful of shows or channels, as the average cable channel lineup stretches into the hundreds.

Younger consumers remain firmly at the leading edge of this trend, as many of these viewers have never subscribed to cable. Today, 60 percent of adults 18-34 are cordless, and it’s a good bet that this ratio will only balloon as members of the mobile-centric Gen Z graduate to adulthood.

Perhaps surprisingly, this 18–34 demographic is not averse to TV advertising, despite having grown up with ad-free services such as Netflix. In fact, a whopping 80 percent of 18 to 34-year-olds are streaming AVOD or vMVPDs every week.

Still, it’s important to note that streaming and traditional TV viewing in the U.S. are not mutually exclusive. In fact, 77 percent of U.S. TV viewers who are keeping their cable subscriptions are also consuming streaming content, moving seamlessly across the two formats.

Majority streams

Respondents who stream at least an hour of content per week: Eight in ten (80 percent) U.S. 18 to 34-year-olds stream AVOD or vMVPDs every week – Source: The Trade Desk and YouGov, May 2021

As TV consumption increases, consumers increasingly jump from platform to platform fluidly to get their fix

The cumulative effect of the proliferation of screens and offerings is that people are more drawn to TV than ever: 49 percent of U.S. TV viewers say they’re watching more TV since the pandemic began.

That is, in part, driven by the sheer accessibility of TV today. For instance, 25 percent of respondents say they on average watch TV on two devices — while 20 percent said they typically stream shows on five different screens.

And while jumping from platform to platform, TV viewers appear inclined to switch viewing modes frequently. Not long ago, many consumers required separate devices or connection paths to access streaming content versus live TV and on-demand viewing. Today, most TVs sold are smart TVs — with streaming apps and linear viewing baked into the same interface and the same remote control — which makes switching between viewing experiences more seamless.

Ad-supported CTV is surging as SVOD nears its ceiling

If 2020 was the year where CTV became a much bigger part of homebound American lives, 2021 is when regular CTV viewing becomes an ingrained habit. This dynamic is only likely to continue as more broadcasters launch new ad-supported streaming services, such as Paramount and HBO Max with ads, who are joining the wide range of platforms that have already reshaped the TV landscape.

As viewing figures grow, these platforms are investing in new content to attract new eyeballs. For example, Amazon (with IMDb TV and, potentially soon, the deep library of content from its intended acquisition of MGM Studios) has reported big jumps in ad-supported streaming, and as a result, is investing in original content. The same goes for Tubi, which parent company Fox says will soon carry more ad inventory than its broadcast network brethren. Meanwhile, in April, ViacomCBS reported that its free streaming platform Pluto TV had added 6 million new monthly users, pushing it past the 50 million marks.

The increased availability of free ad-supported streaming may be helping more people determine just how many services they are willing to pay for. According to our survey with YouGov, the total monthly spending threshold for many is about $20 for streaming services, with nearly half (47 percent) of U.S. TV viewers (cordless and not cordless) unwilling to go beyond that investment. Nearly two-thirds (64 percent) of TV viewers will not spend more than $30 a month on streaming services.

Interestingly, given the mixture of paid and free offerings available, the sweet spot for many consumers appears to be a hybrid model, much like Hulu or Paramount+ (formerly CBS All Access). Most U.S. TV viewers (72 percent) prefer either streaming content for free with ads or paying a low monthly subscription fee with a limited amount of commercial time.

Max willing to spend on streaming services

What is the maximum amount of money your household is willing to spend on TV streaming services, in TOTAL, per month? (Source: The Trade Desk and YouGov, May 2021)

- $0 – (i.e., I’m not willing to spend any money on streaming services per month): 15.6%

- $0.01 to $10.00: 10.0%

- $10.01 to $20.00: 20.9%

- $20.01 to $30.00: 17.7%

- $30.01 to $40.00: 10.6%

- $40.01 to $50.00: 9.4%

- $50.01 to $60.00: 6.8%

- $60.01 or more: 9.0%

Advertisers see CTV as being on par with, or even more effective than, linear TV

According to eMarketer, ad spending on CTV in the U.S. is expected to double from 2020 to 2024, netting out at roughly $18.3 billion. Among the marketing professionals surveyed with Advertiser Perceptions for this report, 45 percent said they increased investment in CTV over the last year. This increase in CTV advertising demand is what led this emerging channel to become a leading growth channel in the advertising market last year.

The reasons for CTV’s rapid ascendancy are clear. Not only has viewership soared, but an overwhelming majority of advertisers (90 percent) view CTV as just as effective if not more effective than linear TV. In addition, CTV is seen as a crucial, incremental channel for delivering audiences that are not reachable through traditional TV models. For instance, 28 percent of advertisers noted that CTV reaches younger consumers and cord-cutters, while another 28 percent pointed to CTV’s ability to deliver incremental reach to linear TV as an asset.

Additionally, linear TV continues to decline, as Samba TV reports a 10 percent drop in the daily average of linear-TV viewing households and a 14 percent decline in total linear minutes viewed in the U.S. when comparing Q1 2021 to Q4 2020. Meanwhile, the traditional TV upfront sales process is rapidly evolving. So, even though 71 percent of the advertisers surveyed plan to reduce or maintain the same level of upfront investment this year, their expectations for these annual shindigs have changed — thanks both to the changes in tactics they adopted during the pandemic and their experience in buying and measuring CTV.

Indeed, following a year when TV ad planning was thrust into chaos, many brands have now come to expect the TV market to operate with the same flexibility and real-time decisions as digital media. Just over half of respondents (56 percent) cited having the flexibility to cancel TV plans without penalty as a top priority, while 55 percent say they’re most focused on maintaining the ability to modify their campaigns in-flight when making their 2021 TV commitments. The lead times for TV campaigns are also tightening, as a plurality of advertisers are opting to plan three months out rather than the usual six months or year ahead.

Naturally, advertisers are also pushing to scrutinize the impact of their ad budgets, particularly as the U.S. emerges from a rocky economic period. This is clearly true for TV, as 70 percent of advertisers say their top priority for 2021 TV investments is linking video investments to business outcomes. Again, CTV is seen as excelling on this front: 92 percent of advertisers said that CTV is highly effective at meeting or exceeding their KPIs; more than a quarter (26 percent) say that CTV outperforms linear TV advertising.

All of this is to say that the more brands have gotten a taste of buying TV ads in a data-driven fashion — the precision, the measurement capabilities, the ability to optimize — the more they want these practices to become the norm in this channel. Even among linear TV ad buyers, 40 percent said they were seeking fewer upfront commitments for their brands this year, while 38 percent said they were seeking more of a focus on measurable outcomes.

We’ve run linear and CTV ads with the same content and similar creative length for select campaigns, and looking comparatively, the results on CTV have been higher in terms of brand favorability metrics. – Karyn Johnson, Chief Investment Officer, Samsung, Publicis Media during a 4A webinar.

Advertisers prioritize measurement on TV commitments

As you are making 2021 TV commitments, which is your top priority? (Source: The Trade Desk and Advertiser Perceptions, May 2021)

| Base: Total Respondents (150) | Rank 1-3 |

|---|---|

| Flexibility to cancel without penalty | 56% |

| Agility to modify campaigns quickly in-flight | 55% |

| Ability to connect investments to measurable business outcomes | 70% |

| Competitive pricing | 63% |

| Access to premium content | 57% |

Advertisers increasingly buy TV ads as part of a holistic strategy

Many in the advertising industry at large have long been hoping for TV advertising to ‘work’ far more like digital advertising — in terms of the ability to target, to track audiences, and to deliver and swap out custom creative as needed. The CTV revolution has given TV advertisers the first real taste of this vision and they clearly want more.

Increasingly, brands are looking to bring their siloed TV buying practices together, both to conduct a more unified, integrated strategy, as well as to make TV advertising as data-driven as the rest of their media buying efforts.

Given CTV’s strategic importance, 50 percent of the advertisers surveyed say they are taking steps to ensure their teams are fluent in both linear and CTV ad-buying approaches rather than hiring new teams.

Of course, the promise of such integration has major consumer benefits, too. Over half (56 percent) of subscription streaming consumers, for example, complained about seeing the same ads repeated — again and again.

A big reason this frequency issue persists is that the average media buyer executes TV ad buys with eight linear partners and eight different CTV providers. In many cases, each of these partners has its own distinct set of data parameters and measurement capabilities, which can make it challenging for buyers to reconcile how many distinct viewers they are reaching with campaigns across outlets, let alone how often they are reaching these people.

Solving that challenge through integrated, cross-channel measurement will not only pay off on the promise of data-driven decisions and precision, but it will also improve the viewer experience and increase the value of relevant advertising.

Increased control is a media person’s dream…this consolidated approach really has given us more comprehensive measurement across channels, and it offers transparency. We can make better, more informed investment decisions…This is the ultimate in real-time data-driven marketing. – Amy Good, Integrated Media Director at The Hershey Company during an Adweek webinar.

Sports become far more accessible through CTV

The cable television industry has long clung to live sports as a primary reason for consumers to maintain their subscriptions. But as streaming becomes the more predominant form of viewing, and more live sports become available on CTV apps and services, those assumptions are being upended.

For example, one-fifth of TV viewers say they plan to stream part of the upcoming Summer Olympics in Japan, while a solid 25 percent indicated they plan to watch NFL games via streaming platforms. Earlier this year, the Super Bowl — synonymous with live broadcast TV viewing — saw its traditional TV ratings dip. However, according to CBS, the Big Game pulled in an average of 5.7 million streamers per minute, a surge of 68 percent when compared to 2020.

Surge in sports streaming

Respondents who stated they primarily watch sports games outside of linear TV (Source: The Trade Desk and YouGov, May 2021)

- 65%: US Sports Viewers 18–34

- 44%: US Sports Viewers

Live sports provide a tremendous environment for our clients’ brands to live within based on the attention and immediacy of the games. The availability and growth of programmatic live sports make for an exciting environment because brands can be involved in the drama as it happens. We can also easily ‘double down’ on our ad support when games go into overtime or when nail-biters and underdog upsets happen by dynamically serving creative to unique audience sets when the audiences start to pop. – Susan Schiekofer, GroupM Chief Digital Investment Officer

Today, 57 percent of Americans say they watch sports once a week — and 44 percent of sports viewers are watching these games outside of linear TV. This figure climbs to 65 percent among adults 18 to 34, as younger people are far less inclined to flip on traditional TV networks to get their sports to fix.

Meanwhile, Amazon next year will take over an exclusive weekly NFL package, which should further accelerate this shift. This comes on the heels of NBCUniversal’s Peacock offering live Premier League games, while the Champions League has its final airing on CBS and streaming on Paramount+. Sports streaming platform FuboTV is also an option to watch topflight matches between Europe’s leading soccer clubs.

Given these changes in how live TV events are consumed, marketers are planning to adjust their spend strategies around key television events. In fact, 74 percent of marketers report that buying CTV ads in conjunction with live sporting events can be more cost-effective and impactful than classic sports sponsorships.

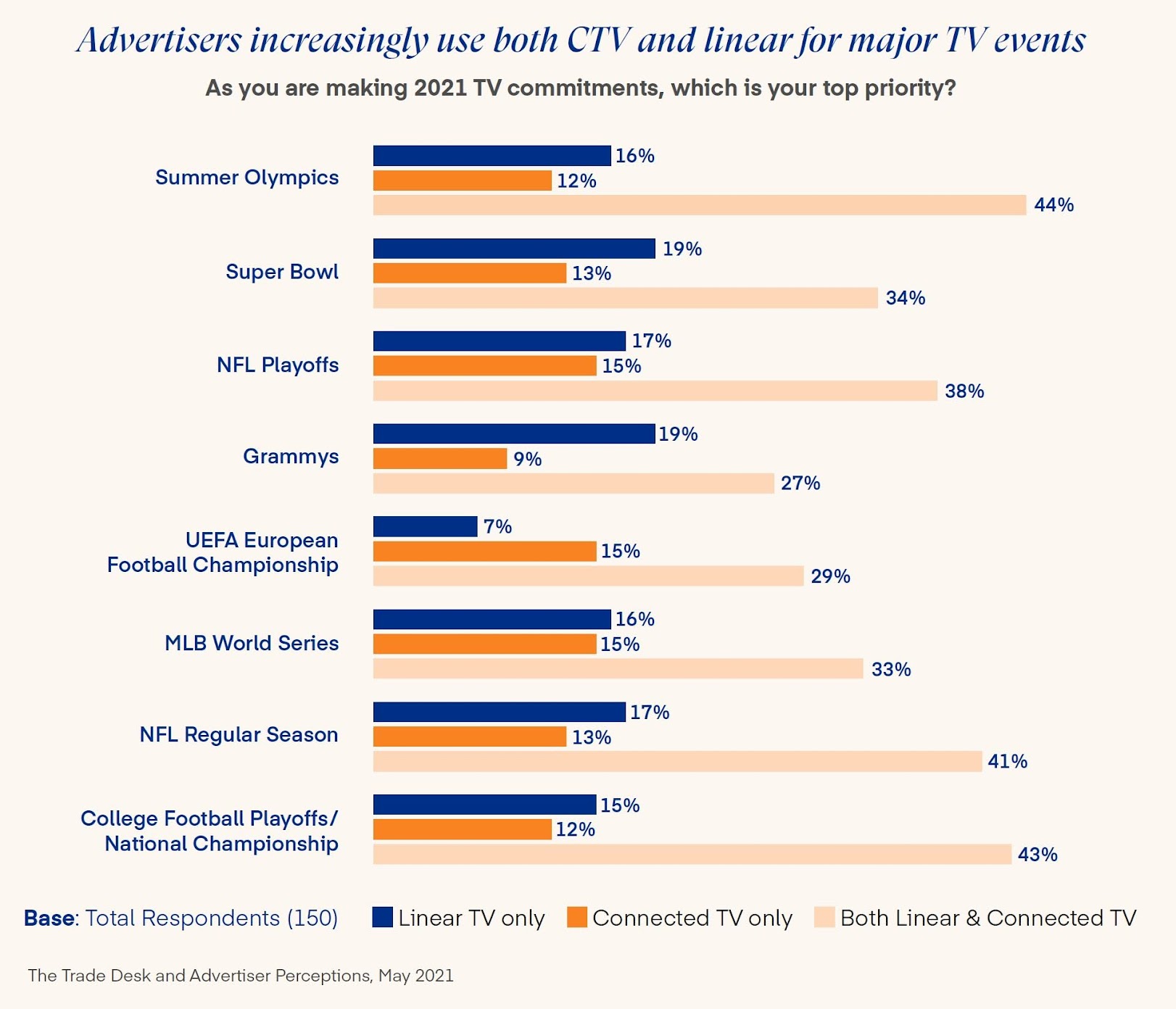

Case in point: 15 percent of U.S. advertisers at this summer’s UEFA Championship plan to leverage CTV exclusively during this event, versus just 7 percent who plan on strictly advertising during the linear broadcast. Even more revealing, a significant portion of advertisers plan to combine linear TV with connected TV for upcoming marquee television events like the Summer Olympics, College Football Playoffs / National Championship, and NFL Regular Season games.

Advertisers increasingly use both CTV and linear for major TV events

As you are making 2021 TV commitments, which is your top priority? (The Trade Desk and Advertiser Perceptions, May 2021)

Connected TV and linear TV move closer together

There has been much discussion over the past year about what the “new normal” will look like, as consumer behavior — everything from everyday shopping habits to entertainment patterns —shifted rapidly. TV viewing in particular was seen as reaching a tipping point, driven by accelerated streaming and on-demand viewership.

It appears clear that, from a consumer perspective, the new normal in television has settled in, and we have passed a tipping point. Streaming is simply becoming synonymous with television viewing for the majority of Americans. Linear television does continue to play a key role, as people have grown comfortable in switching between TV delivery vehicles frequently. But overall linear viewership remains in decline, as consumers abandon pay-TV subscriptions in droves. The “cordless viewer” is becoming the primary TV consumer, and younger generations are only moving further away from traditional TV habits. In fact, much of the rationale for hanging onto the old model, such as access to live sports, is fading as streaming distribution explodes.

However, as cordless viewing normalizes, the TV advertising business still finds itself racing to catch up to this new reality. Advertisers have already demonstrated a strong inclination toward moving budgets to connected TV, and the ad offerings in that channel continue to multiply. At the same time, linear TV still accounts for a healthy amount of viewership and ad inventory. The next 12 months will see brands looking to balance both budget allocation and measurement as they strive to plan and buy a TV as a single platform.

Hanging over this transition of course is the increased pressure on all forms of media to prove its efficacy through a combination of research and tangible data. Indeed, TV is increasingly being measured against digital media, and CTV is viewed as a solution offering many of the benefits of digital advertising, such as precise targeting and the ability to optimize.

In many ways, it feels as though the TV advertising industry is on the cusp of attaining its long-desired holy grail: delivering powerful branding messages using sight, sound, and motion via big screens, while also delivering specific ads to particular audiences brands care about. The faster the industry can work through its various logistical and technological hurdles to bring that desire to fruition, the faster CTV will emerge as one of the most viable ad vehicles for brands, and viewers.