Decrease Payment Processing Fees and Increase Your Sales Throughput While Being PCI Compliant. Getting locked in with a single Payment service provider (PSP) can lead to loss of flexibility, higher payment processing costs, lost sales due to false-positive declines, and loss of control over payments data – putting a strain on revenues. Fortunately, payment optimization is an easy-to-integrate remedy to vendor lock-in.

Read this article to learn:

- How to gain control over your payments strategy and deliver a better experience with all the features and payment methods you need

- Why payment optimization reduces payment processing costs by routing to the best provider for each transaction, based on card type, geography, cost, and more

- How adopting payment optimization enables merchants to maximize payment transaction throughput by minimizing false-positive declines

- The advantages of gaining ownership and portability over payments data by avoiding vendor lock-in

Table of Contents

The Basics of Payment Optimization

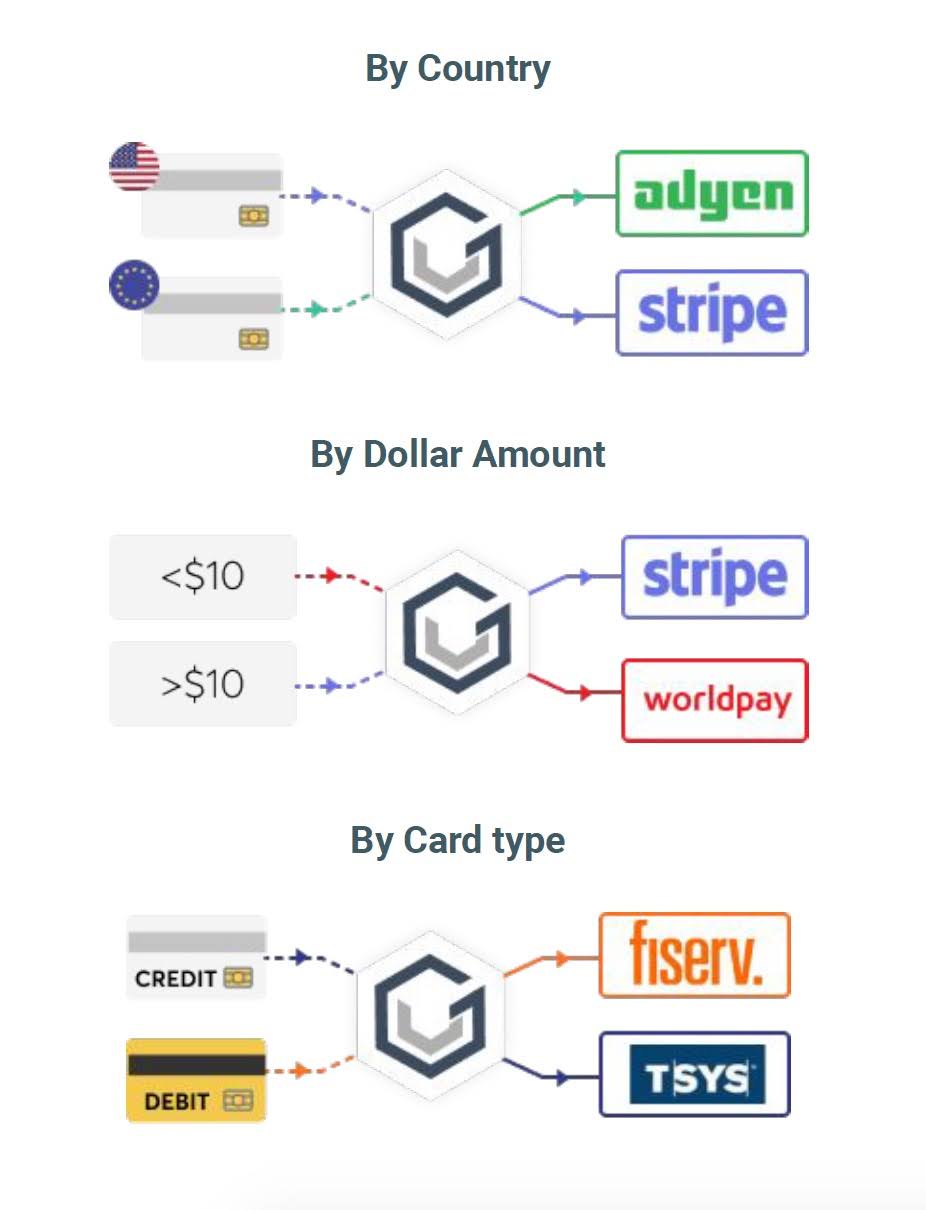

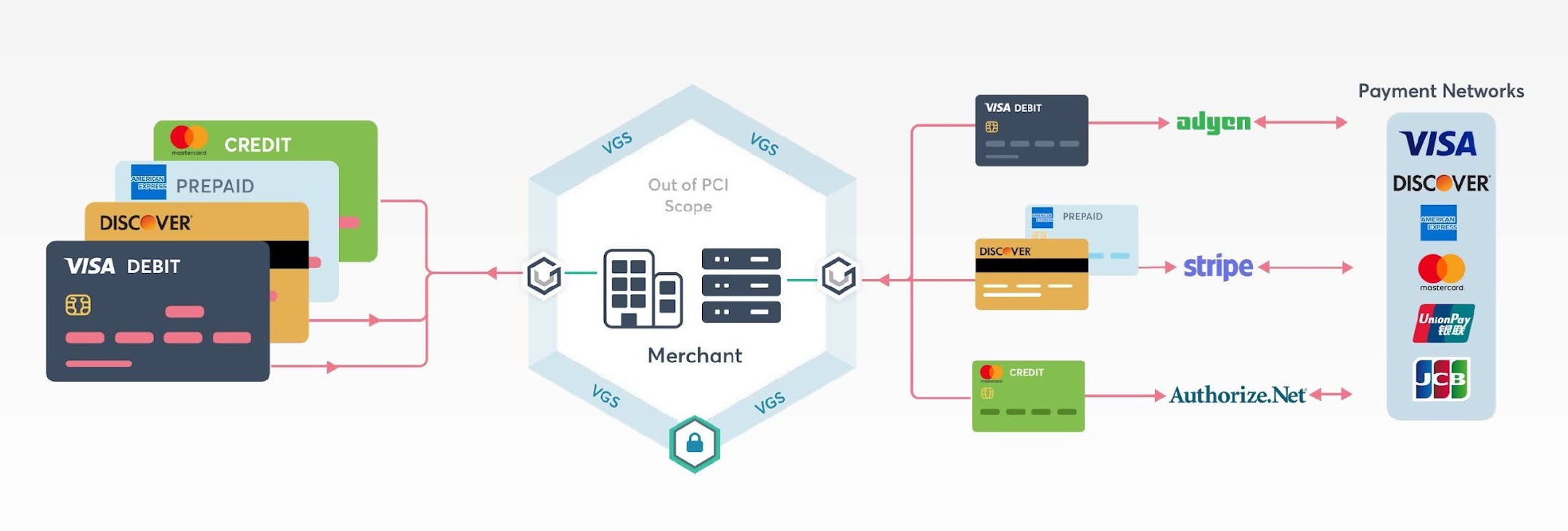

The VGS Payment Optimization solution enables merchants to route their payment transaction traffic to any endpoint for payment processing. This is accomplished with VGS merchants smart routing agnostic aliases (an advanced type of token) in place of the payment transaction details to the endpoint of choice. The routing logic of the alias can be pre-determined by several factors that include, but are not limited to the amount, time, card type, geo-location, currency, or card network. This capability unlocks the merchant’s ability to develop and deploy a robust payment strategy that leverages multiple payment service providers or gateways simultaneously.

Reduce Your Payment Processing Costs

According to the Federal Reserve Bank of San Francisco, 62% of purchase transactions in 2018 came in the form of card payments (credit, debit, or prepaid) while cash represented 26% of transactions and tends to index higher in small-dollar transactions.

As a result, the cost to process card payments has grown as a part of a merchant’s operating costs.

For merchants who operate on a 15% profit margin, transactions involving card payments, the processing fees could reduce their profit margin by 20% if they are paying 3% of processing fees. The swelling costs to process card payments reached a boiling point in 2011, the Durbin Amendment was enacted to cap the Interchange Reimbursement Fees (IRF – card processing fees paid to issue banks) for debit card transactions. Unfortunately, this cap did not apply to credit card interchange fees or the fees that Payment Service Providers (PSP) can charge a merchant. A PSP will typically take the IRF and add a markup to the merchant which it terms Merchant Discount Rate (MDR) or otherwise known as the payment processing fees.

Understanding how IRF rates are set and how your payment process fees are set can be a daunting task. IRF is generally determined by the type of merchant (also known as your Merchant Category Code – MCC) you are. Card networks (Visa, MasterCard, Amex, and Discover) will also set a different IRF for each respective MCC. To make it even more confusing, a merchant with a retail MCC has multiple IRF rates that can be assigned depending on the type of MasterCard credit card used for the transaction. This is also the case for each credit card network. To clear up the confusion, PSPs have come up with easier to understand payment processing pricing. As a result, the markup plus the interchange fees will vary by PSP. Below is a short general description of the 4 major pricing models used in processing payments.

Each has its pros and cons:

Interchange Plus

This breaks down the charges going to the issuing bank and credit card associations, allowing you to see the interchange rate + markup they’re charging you for processing your transaction.

Analysis: This is the most transparent pricing model, but can be very confusing to understand your true cost.

Subscription

You’ll still pay the interchange rates that go to the issuing banks and credit card associations, but instead of paying a percentage markup to your processor, you’ll pay a monthly membership fee and a fixed per-transaction charge.

This pricing model is targeted mainly at smaller-sized penchants who process less than 1MM transactions annually.

Analysis: Depending on the nature and size of your business, this pricing model can potentially result in even lower overall costs than interchange-plus pricing. Your overall effective costs can be even more confusing to understand as your membership fee is based on the volume of payments processed.

Flat pricing

Flat pricing is similar to tiered pricing, but the three tiers are blended into a single flat rate for all transactions.

Analysis: The lack of a monthly fee can make it more affordable overall for small or seasonal businesses. This is the easiest pricing model to understand your cost as it is fixed regardless of the type of transaction.

Tiered Pricing

For simplicity, tiered pricing simplifies processing rates into three basic tiers: qualified, mid-qualified, and non-qualified.

Analysis: Tiered pricing along with flat pricing is the least transparent, but can be easy to read when the bill comes.

DID YOU KNOW?

Did you know that you are not required to use one PSP exclusively? With the VGS Payment Optimization solution, you can use multiple PSP to process your payments. Not only will VGS Payment Optimization route your payment transactions to multiple PSPs, but you can set the logic on how the payments get routed based on several factors. These factors include, but are not limited to the amount, time, card network, card type with a network, geography, etc. Below is a chart that compares three PSPs based on their publicly published rates (as of April 15th, 2020) for an online card purchase of a retail merchant. As you can see below, the PSP that provides the best pricing will vary depending on two-dimensional factors: transaction amount and card network.

Just as a consumer can pick and choose how to pay for each purchase, you should be able to pick and choose how you want to process each transaction. Based on the publicly published fees from a couple of PSPs, you may want to route based on best pricing assuming all else is equal between the PSP providers above.

For a $200 debit card purchase, you may want to route the transaction to Adyen to process, but for a $200 Amex card transaction, you may want to route it to Stripe. For a 20 dollar Amex transaction, the processing cost is negligible between Adyen and Stripe, but you may want to pay a little more for a small-dollar Amex transaction because Stripe has a lower rate of false-positive declines. Please keep in mind that these are illustrative examples based on publicly published pricing.

Don’t get locked into paying higher fees when you don’t have to. Start reducing the payment processing fees you pay now with the VGS Payment Optimization solution. Although on a single transaction, the saving per transaction may not seem much, but when you scale to higher transaction levels, you’ll see the cost savings grow to levels where it does matter.

Maximize Payment Approval Throughput

Maximizing approval rates is a challenge for both issuers and merchants. While the industry struggles with the growing losses due to card fraud, it also has to grapple with lost sales due to a false positive decline. This is a constant battle that the industry is balancing. Tighten up the fraud strategy to decrease fraud and lose sales resulting from false-positive declines, or loosen the fraud strategy to increase approvals and sales while also increasing fraud losses? According to Lexis Nexis, 25% of all declined transactions were false positives and according to Card Not Present 42% of shoppers that get a decline abandon their cart.

According to Payment Journal (June 6, 2019), tokenization has helped reduce false-positive declines by 5% to 8%. VGS Payment Optimization takes that further by allowing you to take a multi-prong approach. You can apply intelligent routing of your transaction without increasing your risk of fraud. With our Payment Optimization, you can optimize your routing to avoid gateways that are experiencing peak hours or route transactions to gateways that are optimal for certain types of transactions to be approved. Qualifying transaction routes can be determined by any type of factor that is captured in the payment data such as location, currency, amount, time of day, etc. This will result in a decrease in false positives that results in a higher approval rate thereby increasing your sales throughput.

Payment Optimization also enables merchants to simultaneously partner with multiple localized payment gateways that support both card and non-card local payment methods. By offering both local payment methods and global card payment methods, it makes expansion into new markets that much easier. According to Forbes (Nov 2018), US merchants selling into the EU, missed out on €1.3bn in potential sales because customers abandoned their purchase due to their preferred payment method not being available. Research commissioned by Stripe in Q3 2018, ‘increasing acceptance of local payment options’ emerged as a top-five challenge for retail executives tasked with orchestrating payment acceptance.

With VGS Payment Optimization, you can grow both globally and locally as you expand your business. VGS supports over 200+ payment providers that provide not only globally recognized electronic payment methods but also localized methods such as SOFORT or Giropay (Germany), WeChat Pay or Alipay (China), and Paylib (France). VGS Payment Optimization enables your business to leverage as many payment providers to ensure your business supports the widest range of payment acceptance so that it does not lose out on any purchases due to the preferred local payment method not being offered.

Control Your Destiny

With VGS’ Payment Optimization solution, we flip that paradigm for you. Not only do we help protect your payment transactions and send them to the endpoint of your choice, but you still own all of your data. Without VGS, if you ever decide to change payment service providers or payment gateways, all the payment transaction data stays with them. If you are fortunate enough to sign a contract to retain your data, you need to engage in a costly data migration project that could last months to migrate from one service provider/platform to another service provider/platform.

With VGS, you choose if your redacted data is stored either in our environment or an environment of your choice. Either way, you own the data. So, when you do choose to change platform/service providers, it only involves integrating with the new vendor of choice and updating your business logic to route a transaction to the endpoint of your choice. With this freedom, you can engage with as many payment gateways or service providers of your choice simultaneously and/or terminate your relationship with them when your contract expires without the feeling that you are locked in and forced to renew when you have found another vendor that better meets your business needs.

Ease of Integration

Deploying your payment strategy is made simple with the VGS Payment Optimization solution. VGS’ Payment Optimization solution has a single point of integration for all your inbound payment requests making it an easy one-step implementation effort that can be ready in days. On the outbound side, VGS supports over 200+ payment gateways and payment platforms (and growing weekly). If your preferred gateway is not on our list, VGS will work with your preferred vendor of choice to support them. With this vast menu of supported vendors and integration into your vendor of choice, all you have to do is come up with your business logic in how and where you want to route all your payments for processing. The additional benefit you get from the VGS platform is that you can instantly become PCI level 2 compliant which we will highlight later.

PCI in a Box

The fastest way to achieve PCI Compliance is to make sure that payment card data never touches your servers. Our Zero Data approach can accelerate your efforts to become PCI compliant by taking all PCI, PII, and sensitive data off your hands so you don’t even need to touch it. With the implementation of the VGS platform, you can get PCI level 2 compliance instantly. With a little more effort you can get PCI level 1 compliance in as little as 21 days. Unlike other PCI or Tokenization offerings, VGS provides not only a PCI-compliant environment but also secures sensitive data both at rest and during transmission. VGS does not stop at just making payment data transmission and storage PCI Compliant but also ensures that you have a solution that can protect any sensitive data or PII that is not covered by PCI but may be required to be protected by other regulations such as GDPR, HIPAA, and CCPA.

With and without VGS

Summary

VGS is more than your technology provider, we can be your strategic partner for your business.

- VGS can help you increase your profit margins by reducing your payment processing costs

- VGS can help you grow your revenue by maximizing your payment transaction throughout

- VGS can help have full control over your data and routing while minimize vendor captivity

- VGS makes integration simple with single point of integration and supports any end point with 200+ pre-established payment providers and gateways

- VGS can help you achieve PCI level 2 compliance upon integration and Level 1 compliance in as little as 21 days