“Just Keep Buying” by Nick Maggiulli is a game-changer in personal finance. This powerful book challenges conventional wisdom, offering proven strategies to save money and build wealth. Maggiulli’s insights are both refreshing and practical, making it a must-read for anyone seeking financial independence.

Dive into this review to unlock the secrets of smart investing and discover how “Just Keep Buying” can transform your financial future.

Table of Contents

- Genres

- Review

- Introduction: Learn how to make money work for you.

- The first rule of saving? Save more when you’re earning more.

- Take stock of your money to get a realistic savings target.

- Want to grow your income? Just keep investing.

- Debt isn’t as simple as it’s made out to be.

- You can’t save all your money, so learn to enjoy spending it.

- Fear #1: The market has peaked, and it may never recover!

- Fear #2: The market is crashing! I’ll wait for things to get better before I buy…

- Summary

- About the author

- Table of Contents

Genres

Personal Finance, Investment Strategy, Wealth Management, Financial Planning, Money Saving, Behavioral Economics, Financial Independence, Retirement Planning, Asset Allocation, Financial Literacy, Money, Business, Personal Finance, Currency, Self Help, Psychology, Productivity, Personal Development

“Just Keep Buying” presents a counterintuitive approach to wealth building. Maggiulli argues that consistent investing, regardless of market conditions, is key to long-term financial success. He debunks common myths about timing the market and emphasizes the importance of regular contributions to investment accounts.

The book is divided into two main sections: saving and investing. In the saving section, Maggiulli introduces the concept of “savings rate” and explains how increasing it can significantly impact wealth accumulation. He provides practical tips for reducing expenses without sacrificing quality of life.

In the investing section, Maggiulli advocates for a simple, low-cost investment strategy focused on index funds. He explains why this approach outperforms most active management strategies over time. The author also addresses psychological barriers to investing and offers strategies to overcome them.

Throughout the book, Maggiulli uses data-driven analysis to support his arguments. He presents complex financial concepts in an accessible manner, using real-world examples and anecdotes to illustrate key points.

Review

“Just Keep Buying” stands out in the crowded field of personal finance books. Maggiulli’s approach is refreshingly straightforward and backed by solid research. His writing style is engaging and conversational, making complex financial concepts easy to grasp.

The book’s strength lies in its practical advice. Maggiulli doesn’t just tell readers what to do; he explains why and provides actionable steps. His emphasis on the importance of savings rate is particularly valuable, as it’s an aspect often overlooked in personal finance literature.

One of the book’s most compelling arguments is for consistent investing, regardless of market conditions. This advice can help readers avoid common pitfalls like trying to time the market or panicking during downturns.

While the book offers excellent advice for beginners, experienced investors might find some sections basic. However, even seasoned investors can benefit from Maggiulli’s unique perspectives and data-driven insights.

The book could benefit from more detailed case studies or a step-by-step guide for implementing the strategies. Additionally, some readers might find the focus on U.S. markets limiting.

Overall, “Just Keep Buying” is a valuable addition to any financial literacy library. It offers a solid foundation for building wealth and challenges readers to rethink their approach to saving and investing. Whether you’re just starting your financial journey or looking to optimize your existing strategy, this book provides valuable insights and practical advice.

Introduction: Learn how to make money work for you.

Just Keep Buying (2022) is a no-nonsense guide to personal finance that delights in busting myths and dispelling old clichés. Tackling all-important questions like saving and investing, it digs into the psychology behind money and provides a realistic guide to making sound financial decisions.

If there was just one factor you could use to guide your investment decisions, it should be: Most markets go up, most of the time.

In the last one hundred years, despite a great depression, two world wars, the threat of nuclear war, and a great financial crisis, the stock market in the United States increased 160,000% from 1922 to 2022 after adjusting for inflation. With such a robust and consistent increase in the value of the stock market over time, there might be no better investment advice than “Just. Keep. Buying.”

But for most people, continually investing in a volatile stock market is terrifying. As the famed financial author Jeremy Seigel said, “Fear has a greater grasp on human action than does the impressive weight of historical evidence.”

There’s a lot of bad advice out there when it comes to money. The problem isn’t just that a lot of what we’re told about personal finance relies on bad data, though.

Often, that advice relies on sweeping assumptions about what’s “good” and “bad” for everyone. But decisions around finance, author Nick Maggiulli argues, are usually context-dependent.

Credit card debt, for example, can actually be a useful tool for some people. And seemingly frivolous expenses, like buying a daily coffee, can be a waste of money in some cases – in others, though, those spending decisions can contribute to a fulfilling life. It’s the same with saving. How much money should you hold onto? It really depends on how much you’re making.

As we’ll see in this summary, you can only make informed calls on these issues when you know more about the individual people involved. It’s a simple message, but it’s one that’s worth hearing. The thing about all that bad advice is that it doesn’t just fail to help you manage your finances – it’s also often the source of guilt, stress, and anxiety.

So let’s take a different approach. One that’s grounded in life’s messy realities, not some wishful idea of how things should be. One that actually helps you.

In this summary, you’ll also learn:

- what an Alaskan fish can teach you about saving;

- why it’s worth investing in sluggish markets; and

- how to spend money without feeling guilty.

The first rule of saving? Save more when you’re earning more.

We’re going to be talking about money in this chapter. But our journey doesn’t start on Wall Street or the trading floors of London and Frankfurt. Our first stop is southern Alaska.

We’re in the world’s largest temperate rainforest. Anglers prize this area for its clear streams, which are filled with large, trout-like fish known as Dolly Varden charr.

These Pacific streams contain little sustenance – until the early summer. That’s when salmon laden with eggs arrive. Charr love these eggs, and what follows is a months-long feeding frenzy. But then the salmon leave. The streams once again become a food desert.

For years, biologists couldn’t figure it out. There just weren’t enough calories to support so many charr year round. Yet there they were, month after month – hundreds and thousands of thriving fish.

So how does it work? The answer is phenotypic plasticity – a species’ ability to adapt its physical form to suit its environment. Dolly Varden charr shrink their digestive organs and slow their metabolism when there’s little food. When the salmon arrive, by contrast, those organs double in size and their metabolism speeds back up.

So what’s that got to do with finance? Quite a lot, actually. Adapting your behavior to your environment also holds the key to saving.

Let’s break that down. Google the question, “How much should I save?” and you’ll get 150,000 hits with very precise answers. You should save 20 percent of your income, one self-proclaimed expert claims. No, another says, you should have three times your income saved by the age of 40.

All of those answers share an assumption – that everyone has the same ability to save. That’s just not true, though. As economists point out, the biggest determinant of savings is income. In the United States, folks in the bottom 20 percent of earners typically save just 1 percent of what they earn. For the top 20 percent, that rises to 25 percent. The idea that everyone should save X amount flies in the face of empirical evidence, which shows that not everyone can.

And the thing is, lots of people move up – and down – those income brackets. Life, after all, isn’t static. Often, you’ll earn less when you’re young and more when you’re older. But high earners also quit the rat race to take on more fulfilling work in less well-paid industries. Some jobs force you to live in expensive cities; others don’t. Then there are life’s highs and lows and their financial consequences – marriages and divorces, children, promotions and layoffs, leaking roofs and Christmas bonuses. To find a single, neat rule that covers so much messy reality is a fool’s errand.

This brings us back to our Dolly Varden charr, which lower and raise their caloric intake according to how much food is available. Their maxim? Eat what you can, when you can. And that’s a great principle for saving, too: save what you can, when you can. In practice, that means saving more when you’re earning more and less when you’re earning less.

Take stock of your money to get a realistic savings target.

Let’s recap. We often think about saving as a matter of should and ought. But money doesn’t follow moral laws. It’s mathematical. And it bluntly says you can’t save what you don’t have.

So let’s forget about Google’s questionable insights into what you should be doing and reformulate the question more pragmatically. Where are you financially? What can you save, right now?

To find out, you’ll need to open the books and take a closer look at your money.

Accounting is a famously double-sided thing. One column records money in. The other records money out. Add up everything in the first column, and then subtract the amount in the second. There’s your answer. Savings, in other words, equals income minus spending.

The first column is easy – it’s the number on your paycheck. Outgoings are a bit trickier. The standard advice is to keep track of every cent you spend. If you’ve tried, and failed, to do that, you’re in good company. Even the author can’t do it. Fixed expenses, like rent or mortgage payments and monthly utility bills are easy – they don’t change much. But keeping track of fluctuating expenses is harder.

So here’s how to simplify things: determine your fixed costs, and estimate the rest. Take groceries. You know how often you go shopping and how much you usually spend, so average it out. Say you do a weekly grocery run that usually comes in at around $100. Some weeks, it’s closer to $90. Other weeks, you may need to replace something relatively expensive, like a bottle of nice olive oil. Then it’s nearer to $110. All in all, though, you’re spending about $400 a month.

Now apply that to all your expenses. What, on average, do you spend on going out? On coffee before work? On drinks after work? On fuel or train tickets? On books, or movies, or your hobby? Once it’s down on paper, complete the equation. Say you’re taking home $4,000 after taxes and spend $3,000 on bills and variable expenses. That leaves $1,000. That’s how much you can save.

Is the number you’re left with enough, though? Again, it depends. The general rule of thumb is that you’ll need 25 times your annual expenditure to retire, which is what most of your savings are for. But how that looks in practice comes down to lifestyle. If you’re used to regular foreign travel and a busy social life in an affluent area with high prices, you probably won’t want to give those things up. That means you’ll need more than someone who doesn’t do or have those things.

But let’s say it’s not enough – what then? There are two answers. The first, which happens to be the right one, is the blunt mathematical answer: you need to grow your income, to earn more. That’s a painful realization, which is probably why so much mainstream financial advice focuses on the second answer – gutting your quality of life to save more right now. But that’s a recipe for misery.

Want to grow your income? Just keep investing.

The reason you can’t save yourself rich is simple: you run out of things to cut back on fairly quickly. Put differently, there are hard limits to saving. What about growing your income, though?

There are limits here, but they’re a long way off. If you’re earning $10,000 an hour, it might not make sense to grow your income any further. You’re already set financially, and you might value free time more than the extra money you could be earning if you worked more. Similarly, high earners might forgo raises if that extra money is taxed at a very high rate.

In most cases and for most people, though, growing your income is the way to go. The question is how? The author’s answer is in the book’s title. But before we get to that, let’s talk horses.

More specifically, racing horses. One of the horse racing world’s greatest stars is a man called Jeff Seder. For years, Seder looked at all sorts of criteria before buying horses. He’d check their pedigree and measure their nostril size, or the weight of their excrement, or the density of their muscle fiber. But nothing correlated with racing performance. So Seder tried something different. He measured the horses’ heart size – specifically, the size of their left ventricles. Bingo. Finally, he’d found a reliable predictor of a racing success. He bought more horses with larger left ventricles and won more races.

Sometimes a single piece of accurate information can help us understand a complex system, like the relationship between a horse’s biology and its ability to win races. Or the best way to grow your income in volatile financial markets.

Here’s how Warren Buffett summarizes that single piece of information: most stock markets go up most of the time. He has a point. During the twentieth century, the United States went through two world wars, the Depression, a dozen recessions, an oil shock, and a flu epidemic. But the Dow Jones, a measurement of the value of stocks, rose by 160,000 percent! That’s after inflation, by the way. So what’s the takeaway? Here’s the author’s view: the only investment advice worth following is to just keep buying stocks. Averaged out over decades, it’s much harder to lose than it is to win.

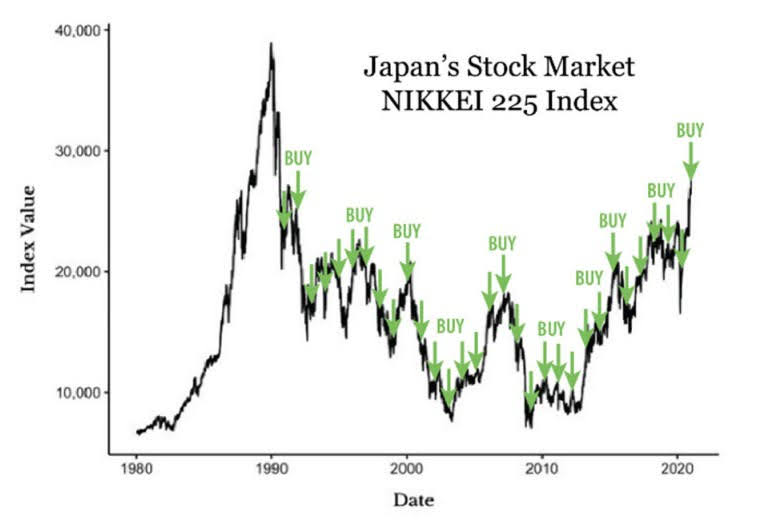

Even famously sluggish markets, like the Japanese stock market, reward this philosophy. Japanese stocks hit their peak in ’89 and still haven’t recovered that level. If you’d made a one-off investment of $1,000 back then, you’d have $690 today. But if you’d invested $1,000 every year between 1989 and 2022, your $33,000 investment would have grown to $59,000. That’s not a great return, but it’s more than you’d have if you’d let inflation eat away at your cash savings.

Of course, you don’t have to wed yourself to a single market. As we said, most markets go up. What you really want to do is spread your investments, for example by buying into an index of global companies operating in multiple markets. We’re not going to get into the technicalities of how to do that here – that’s something you’re better off discussing with your financial advisor. What’s worth remembering, though, is that, historically, the line trends upwards. Hitch your money to that line and you’ll grow your income.

Debt isn’t as simple as it’s made out to be.

In the world’s deserts, there are two kinds of flowering plants – annuals and perennials. Annuals grow, reproduce, and die over a single season, while perennials live for any number of years.

Desert-dwelling annuals do something strange, though. Each year, a portion of their seeds fails to germinate. That’s true even when the conditions are perfect for sprouting.

At first glance, that doesn’t make a lot of sense. This is a harsh environment in which the survival of a species is anything but a given, after all. Why would a plant pass up an opportunity to reproduce?

It comes down to water – or the lack of it. Growing plants need water, but there’s not a lot of rain in the desert. Worse, what little rain there is falls at highly irregular intervals. If every seed sprouted simultaneously, a single drought would kill a plant’s entire offspring and wipe out its lineage. So here’s the evolutionary play: some seeds are held back to sprout later, increasing the chance that the plants’ early growth will coincide with a rare rainstorm.

In finance, there’s a name for this kind of strategy – the kind that’s designed to prevent catastrophic wipeouts in case the future turns out badly. It’s called bet-hedging. Often, it involves a trade-off. For our annuals, keeping seeds back means giving up territory to competitors. But forgoing the short-term reward of territorial expansion isn’t as valuable as the long-term reward of reproduction.

Like those Alaska charr we encountered earlier, the desert plants can teach us something valuable about money. Their lesson for us isn’t about saving, however – it’s about debt.

Common sense says that debt is bad. Period. Even the Bible warns that “the borrower is slave to the lender.” But it’s not as simple as that. In fact, debt can be pretty paradoxical.

Take credit cards. We all know that credit card interest rates are extortionate. That once you start digging with that shovel, it’s easy to end up in a hole that’s hard to get out of. That’s not necessarily wrong, but it’s not the full picture, either. It’s fascinating – credit cards can actually help low-income earners. Economists call it the credit card debt puzzle.

Imagine someone has $1,500 in their checking account and $1,000 in credit card debt. The best play is to pay off the debt and make do with $500, right?

Let’s return to our annuals. At first, their behavior seems irrational. Look more closely, though, and that “irrationality” actually makes a lot of sense. So no – that’s not necessarily the best play.

When you don’t have a lot of money, the future looks pretty daunting: one drought, one spot of bad luck, and you’ll be wiped out financially. Your paycheck can’t handle emergencies. If the car that gets you to work breaks down, you won’t have enough cash on hand to get it fixed. Disaster. You also know that your credit rating isn’t great, so finding a loan isn’t going to be easy either. So what do you do? Well, you keep paying those extortionate interest rates to preserve your future access to credit. You keep some seeds back. You hedge your bets. You ensure financial survival.

That goes to show that debt isn’t really “good” or “bad” – it’s a tool that can be used or abused. It all comes down to context. The real question, then, is this: Does debt help you achieve your goals?

You can’t save all your money, so learn to enjoy spending it.

The cool, calculating rational agents of economics textbooks are a myth. Real humans are messy. Impulsive. More likely to follow the crowd, or the hidden logic of the subconscious, than reason. That means we can’t really talk about money in the abstract. We also have to look at its psychological impact. At how it makes us feel. Which, often enough, is miserable.

Take it from the American Psychological Association, which since 2007 has run an annual survey that identifies the main stressors in Americans’ lives. The topic that tops the list each year? Money. A 2018 study by Northwestern Mutual, meanwhile, found that half of all Americans experience high levels of anxiety around savings. And that anxiety appears to affect everyone, regardless of income. Another survey found that 20 percent of investors worth between $5 and $25 million were also worried about not saving enough!

What explains this epidemic of stress around savings? In a word, guilt.

We’re bombarded with financial advice that makes us second-guess ourselves. Buying a daily coffee? Crazy – you’re literally peeing hundreds of thousands of dollars down the drain. New sneakers? Not if you want to get on the property ladder. Organic peanut butter? If you wanted to retire, you’d buy regular. The underlying message couldn’t have been better designed to trigger guilt. Every cent you spend, it says, could’ve been saved, and if you actually took responsibility that’s exactly what you’d do.

But you can’t save every cent, and trying only makes us sick. When researchers at the Brookings Institute looked at Gallup survey data on savings and mental health, for example, they found that stress around not saving enough outweighs the positive effects of saving. Their conclusion: saving is only beneficial if you can do it in a stress-free way.

Saving, in short, is important – but so is quality of life. So how can you strike the right balance – how do you take care of your finances while preserving your health? Here’s the author’s take: focus on purchases that maximize long-term fulfillment.

A good place to start thinking about fulfillment is the American author Daniel Pink’s book Drive, which looks at human motivation. Pink argues that there are three things which fulfill us – autonomy, mastery, and purpose. In other words, being self-directed, improving our skills, and being part of something bigger than ourselves. Those are great filters to apply to spending decisions.

Take that bugbear of so many financial experts – that latte you pick up from the coffee shop before work. It looks like a frivolous purchase, but maybe that latte allows you to perform at your best at work. In that case, it’s enhancing your occupational mastery. That’s a deeply fulfilling long-term project, which means it’s money well spent. Other frivolous-looking purchases might, on closer inspection, turn out to contribute to your sense of autonomy or purpose.

In the end, money is a tool – it’s what allows you to create a life you want to live. What’s really difficult, then, isn’t spending it – it’s figuring out what you want in life. What do you care about? What would you like to avoid? What kind of values do you want to promote in the world? Once you figure that out, spending money will be both easier and more enjoyable.

Fear #1: The market has peaked, and it may never recover!

A common counterargument to the “just keep buying” investment philosophy is Japan’s stock market performance over the last 33 years. If you invested a thousand dollars in Japan’s stock market in 1989, it would only be worth $690 today. However, if you just kept investing $1,000 in Japan’s stock market each year for the past 33 years, your $33,000 would be worth approximately $59,000 today. Not a great return, but it beats keeping your money in cash and watching it get eaten away by inflation!

But you don’t need to settle for mediocre returns (like Japan’s stock market returns over the last 33 years) if you don’t wed yourself to one market. Remember, MOST markets go up, most of the time, not one market goes up until the end of time.

In any 30-year period, 88% of markets around the world make new highs. Therefore, if you invest in several markets, the chances of your portfolio recovering from a crash in 30 years is almost 100%. An easy way to invest in most markets is to buy a large world stock index like the Vanguard Total stock index ETF (ticker symbol: VT). The total world stock index ETF is a collection of 9,551 stocks in every investible market in the world which automatically replaces dying companies with thriving companies, so you don’t need to manage it. When you diversify in a world index of stocks like VT fund, you’re no longer reliant on one region or one economy succeeding. Instead, you’re investing in human ingenuity and our ability to make businesses and products that earn money over time.

But even in the most diversified stock indexes, you will encounter substantial volatility (huge price swings throughout the year). The S&P 500 (the 500 largest stocks in the US – which makes up the majority of the world index stock holdings) had an average intra‐year price decline of 14% over the last 50 years. However, despite the large intra-year declines, the S&P finished positive at the end of 40 of the past 50 years.

You must tolerate some volatility if you want to grow your wealth, but author Nick Maggiulli says you should not tolerate more than a 15% decline in your entire investment portfolio. History shows that if you avoid a 15% decline by dedicating a portion of your portfolio to income-producing assets like long-term Treasury bonds and specific stock market sectors like energy, consumer staples, and utilities (which have historically risen as the overall stock market declined), you will outperform the overall stock market over time.

Fear #2: The market is crashing! I’ll wait for things to get better before I buy…

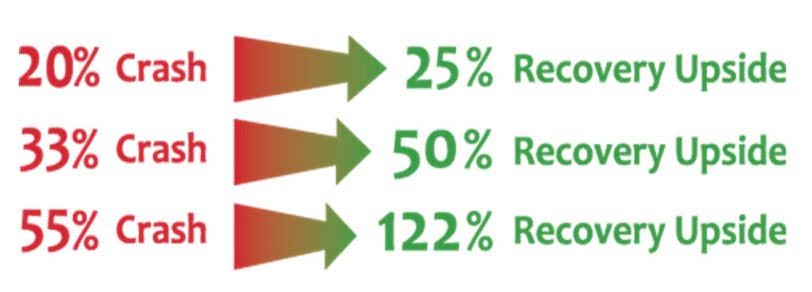

When the stock market portion of your portfolio crashes below 15%, it can feel like your money is being incinerated and it is hard to just keep buying. But if you can find the courage to keep buying stocks when stocks are getting massacred, the money you invest will enjoy supercharged returns when the stock market recovers. If you invest during a 20% decline and the market recovers, you don’t make a 20% profit; you make a 25% profit. Likewise, if you invest when the market is down 33% (like it was in March 2020), you don’t make a 33% profit when the market recovers; you make a 50% profit when the market recovers.

The greater the decline, the greater the upside, and the longer you can wait for the stock market to recover. During the Great Financial Crisis in 2008 and 2009, the market was down 55%. If you bought when everyone else was panicking, you could have patiently waited ten years for the stock market to recover and enjoyed an 8% annual return for ten years. But the market didn’t take ten years to recover, it took four, and those who kept buying as the market bottomed enjoyed a 22% annual return over the next four years.

If you hold off buying, or worse, sell your stocks and get back in the market later, you will likely miss the bottom and need to buy back your stocks at a higher price. Even in a prolonged bear market, like the 1970s, if you missed the ten best days between 1970 and 1980, you would have endured a ‐20% return. But if you stayed invested, you would have received a positive 17% return. And if you were out of the market and holding cash throughout the 1970s, inflation would have eroded your purchasing power by 17%.

Summary

You’ve just finished summary to Just Keep Buying, by Nick Maggiulli.The most important thing to remember from all this is:

How much should you be saving? Spending? Investing? Borrowing? Nick Maggiulli is a realist, not an idealist, which is why he argues that it all comes down to context. How much can you save, or invest? Does debt help you achieve your goals in life, or is it an emergency stopgap? Does spending fulfill you? It’s only when you dig into those questions that you’ll find a viable financial plan that works for you.

Nick Maggiulli is the Chief Operating Officer and Data Scientist at Ritholtz Wealth Management, where he oversees operations across the firm and provides insights on business intelligence. He is also the author of OfDollarsAndData.com, a blog focused on the intersection of data and personal finance. His work has been featured in The Wall Street Journal, CNBC, and The Los Angeles Times. Mr. Maggiulli graduated from Stanford University with a degree in Economics and currently resides in New York City.

Nick Maggiulli | Website

Nick Maggiulli | Twitter

Table of Contents

Introduction

1. Where Should You Start?

I. Saving

2. How Much Should You Save?

3. How to Save More

4. How to Spend Money Guilt-Free

5. How Much Lifestyle Creep is Okay?

6. Should You Ever Go into Debt?

7. Should You Rent or Should You Buy?

8. How to Save for a Down Payment (and Other Big Purchases)

9. When Can You Retire?

II. Investing

10. Why Should You Invest?

11. What Should You Invest In?

12. Why You Shouldn’t Buy Individual Stocks

13. How Soon Should You Invest?

14. Why You Shouldn’t Wait to Buy the Dip

15. Why Investing Depends on Luck

16. Why You Shouldn’t Fear Volatility

17. How to Buy During a Crisis

18. When Should You Sell?

19. Where Should You Invest?

20. Why You Will Never Feel Rich

21. The Most Important Asset

Conclusion: The Just Keep Buying Rules

Acknowledgments

Endnotes