73% of retail professionals said the crisis accelerated some, if not all, of their tech-related investments, putting pressure on them to innovate faster to stay relevant and profitable.

In collaboration with the National Retail Federation (NRF), this article explores how the digital shoppers’ relationship towards technology has shifted since the pandemic, offering retailers and brands insight as to where they should make tech investments.

Read on to learn:

- How technology will shape the future shopping experience

- What consumers want and expect online and in store

- Where retailers and brands are focusing their investments

Content Summary

Table of Contents

Introduction

Online Discovery

Online Purchase

In-Store Shopping

Payments

Delivery and Collection

Conclusion

Introduction

Over the last decade, consumers have become comfortable with technologies being interwoven into the commerce experience. The growing reliance on technology became that much more apparent during the COVID-19 pandemic, as retailers and brands sought to stay connected with consumers as the spread of the virus escalated safety concerns.

The impact of COVID-19 accelerated the digital transformation across the retail industry. Besides ramping up capabilities to better serve consumers in the online channels, retailers also made in-store tech investment to create touchless retail experiences. Almost three-quarters of retail professionals said the crisis accelerated some, if not all, of their tech-related investments, according to Voice of the Industry: Digital Survey.

In collaboration with the National Retail Federation (NRF), Euromonitor International created this report to explore how the digital shoppers’ relationship towards technology has shifted in light of the COVID-19 pandemic, offering retailers and brands insight as to where they should make technological investments today and in the years ahead. This report is organised into five aspects of the retail shopping experience with the order mimicking the typical transaction flow: online discovery; online purchase; in-store shopping; payments; and delivery and collection.

The percentage of retail professionals who say COVID-19 accelerated:

- 72% of the company’s digital transformation by at least a year.

- 73% of the company’s technology-related investments.

- 58% of the company’s new technology-related product launches.

Online Discovery

The pandemic has re-oriented the way consumers shop. While e-commerce was rising in popularity, it largely served a transactional role and stores remained the primary avenue for experiencing a brand or interacting with a product. The purpose of these two channels was evolving, but the crisis gave a temporary preview of a world where the purposes of the digital and physical channels swapped positions. While stores will continue to be a key channel for shopping in the future, this period showed the potential for the digital channel to play a bigger role in the future shopping experience.

Being able to connect virtually with consumers on digital platforms turned the static online experience into a multisensory one, conjuring up the emotions most often associated with in-person interactions. Retailers and brands leveraged digital platforms, technologies like augmented reality (AR) and virtual reality (VR) as well as emerging content mediums like livestreaming to mimic elements of the in-person shopping experience.

Consumer behaviour and motivation

One way to recreate the physical experience in the digital channel is through virtual try-on features. In Euromonitor’s Voice of the Consumer: Digital Survey, which is an annual survey of internet-connected consumers in 20 countries, almost 30% thought the ability to virtually try on was an important online feature. Globally, this sentiment is highest among millennials and emerging market consumers.

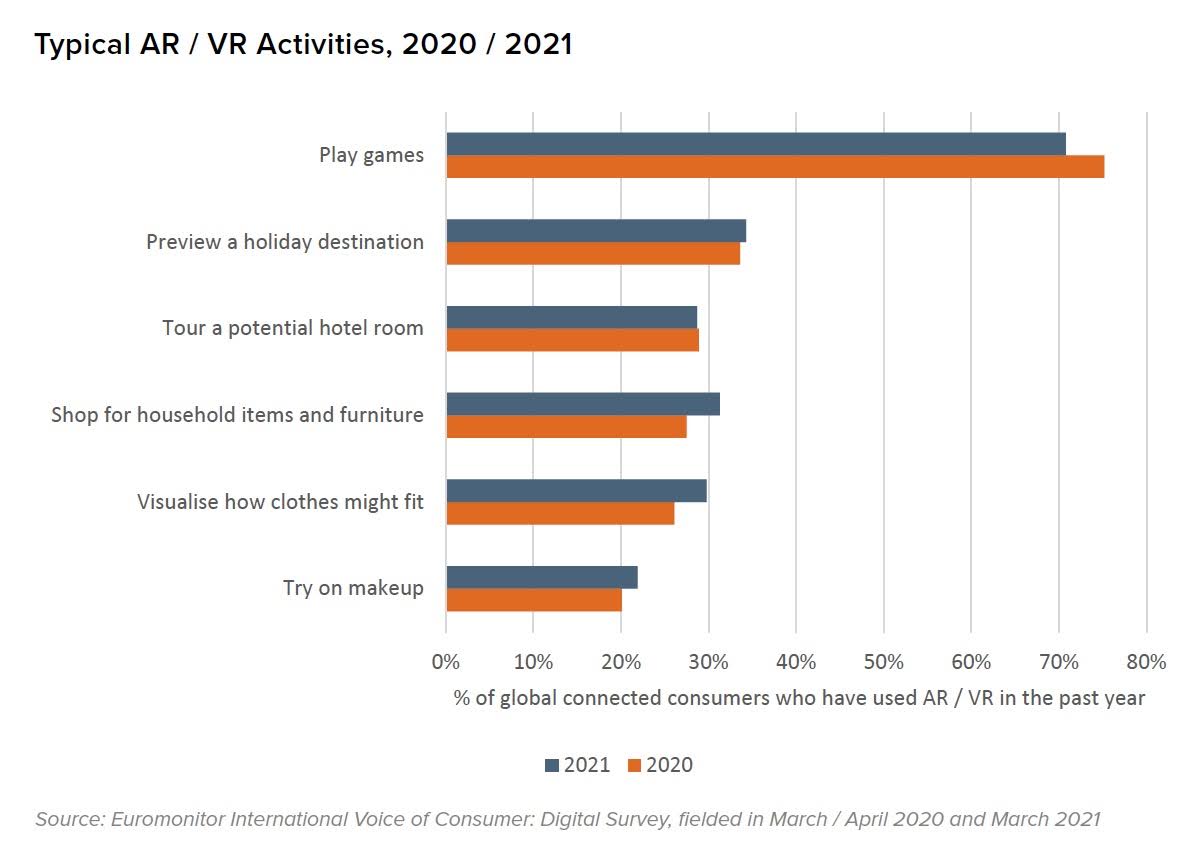

Increased use of technologies like augmented and virtual realities have potential to improve the visual cues of the online shopping experience. Although these technologies have been commercially available for years, 58% of connected consumers globally report not having used either.

From a consumer perspective, gaming remains the main avenue for exploration. Of those that have used AR / VR in the past year, 30% utilised it to shop for household items and furniture as well as clothes. In fact, both figures are up from the 2020 survey fielding as more consumers turned to these technologies to enhance the online experience for these more visual products.

Livestreaming, which gained popularity in recent years as a content medium, made inroads during the crisis due to its ability to create the emotional connection more associated with in-person shopping. Combining elements of streaming video, social media and celebrity into a shopping experience, live selling started to gain traction around the globe as a way for brands to connect with shut-in consumers.

Consumer spotlight

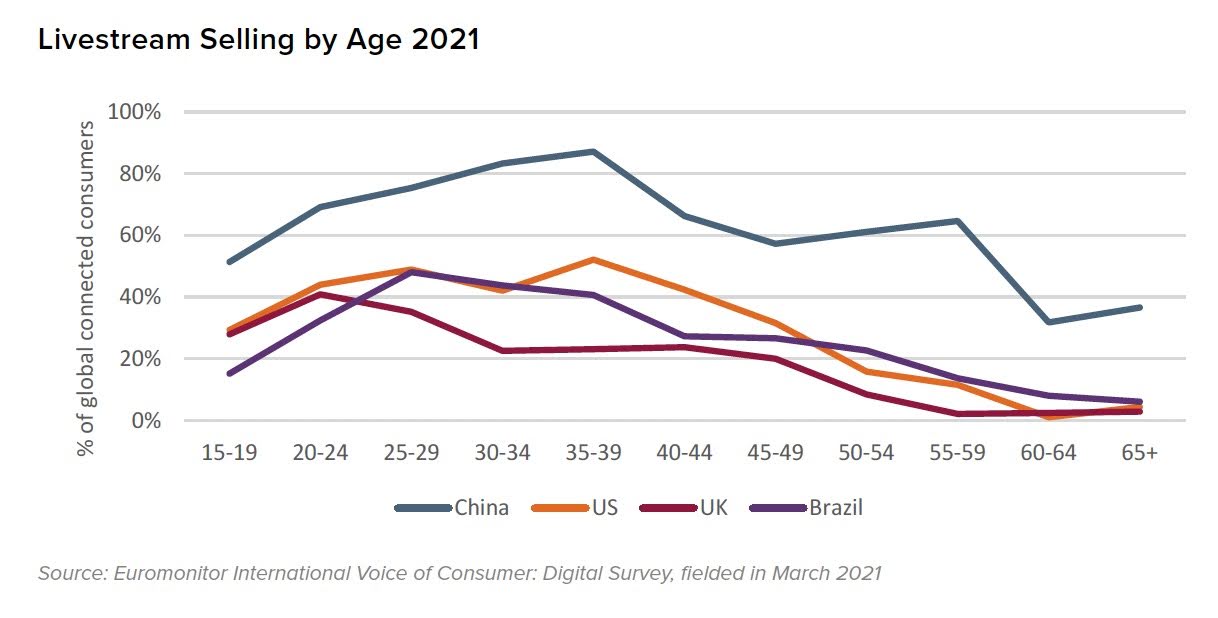

In the March survey, almost 30% of global connected consumers reported using livestreaming to make a purchase in the last month. In general, connected consumers globally say the top reasons they participate in commerce livestreams is to get discounts or more details on the product or service features before buying. Of those who have made a purchase, apparel and personal accessories topped the list with 50% reporting a purchase from that category.

Interest in this emerging retail channel is highest among global consumers between the ages of 21 and 34, peaking with the 30–34 age group with 46% having used this medium to make a purchase. As a nation, China is leading with 63% having made a purchase in the last month, according to the Voice of the Consumer: Digital Survey.

In contrast, that figure is far lower than other markets, sitting at 29% in the US, 28% in Brazil and 18% in the UK, for example. In fact, commerce livestreaming is so mainstream in China that more than half of Chinese connected consumers from 15 to 60 years leveraged livestreaming for commerce in the last month.

While the concept was growing in China before the pandemic, live selling skyrocketed in 2020 due to the limitation placed on in-person engagements. From there, it started to gain traction in Asia Pacific and eventually moved West. In 2020, Amazon opened its Amazon Live to influencers and Facebook added livestreaming capabilities to its Facebook and Instagram platforms. This medium’s popularity will likely continue to grow post-pandemic as the concept takes hold.

Industry perspective and investment

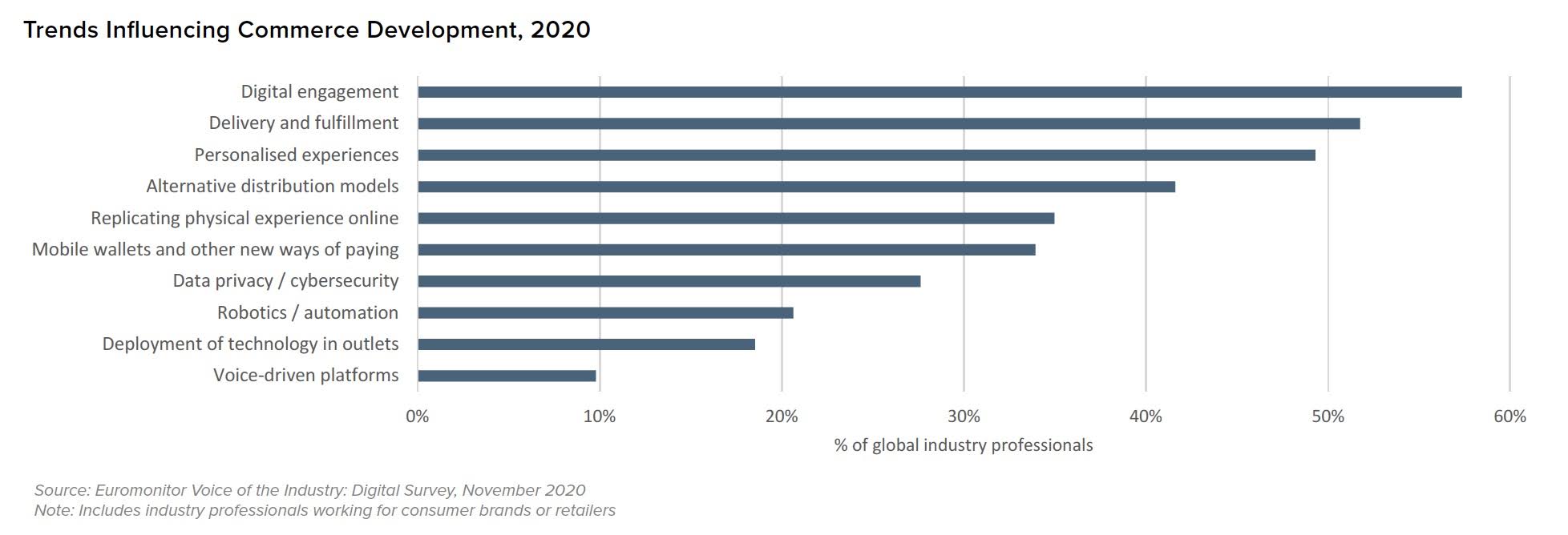

For companies, digital emerged as the default channel for all aspects of life and the key one for engaging with consumers. In fact, 57% of retail professionals viewed digital engagement as the top trend influencing digital commerce development, ahead of other headline-grabbing topics like delivery and fulfilment or robotics and automation.

While going virtual is still in its relative infancy, businesses are experimenting by offering immersive virtual experiences to sell products from clothes to make-up to furniture with the goal of increasing conversions and reducing return rates. These virtual experiences range in level of sophistication. Some, such as online consultations, virtual classes and commerce livestreams, merely connect consumers with a brand via digital platforms. Others go so far as to mimic the experience of physically touching and trying on a product through the use of technologies like augmented and virtual realities.

Case Studies: Inabuggy Canada

Inabuggy, a grocery delivery service provider, partnered with McEwan Fine Foods to launch a 3D virtual shopping experience that allowed customers to tour store aisles online and click on products to view details and add them to the cart.

Case Studies: Ulta Beauty US

Ulta Beauty saw interest in its virtual try-on app, GLAMlab, surge 12x over the previous year as users tried on 171 million shades of cosmetics in 2020. The beauty store chain also added skin analysis tools and more personalised product recommendations.

Case Studies: Alibaba China

Chinese marketplace Alibaba is the undisputed leader when it comes to commerce livestreams. In November 2020, it hosted its 11.11 shopping festival where live streaming accounted for USD6 billion in sales, double the previous year.

Case Studies: Bissell US

US-based cleaning products company Bissell used livestreaming on Alibaba’s Taobao Live to reach Chinese consumers, growing its presence in this key market. Due in part to livestreaming, Bissell tripled its business in China in 2020.

Outlook

Although this approach was used to drive engagement with home-bound consumers, virtual experiences will likely become more commonplace in the post-pandemic era as digital becomes the default channel for brand exploration.

Deriving value by going virtual will depend largely on how well the technology can represent the most meaningful product attributes for customers in context. Given that these attributes differ by industry and category, there will be many tipping points as the technologies that enable these virtual experiences become more common.

Nevertheless, this period has shown how quickly society can evolve. During this turning point, businesses shifted their priorities to further develop virtual capabilities, lowering the barriers for discovery and purchase on the digital channel.

Online Purchase

Euromonitor International estimates that global online sales of products grew by 25% in real terms in 2020. Even though the annual growth rate is expected to fall, e-commerce will continue its ascension as the fastest-growing channel for purchases. The key debate is what proportion of this overnight e-commerce growth is sustainable. Euromonitor projects that e-commerce will account for 51% of the retail industry’s growth globally from 2020 to 2025.

Consumer behaviour and motivation

With many physical outlets temporarily closed, many consumers turned to online shopping for the first time. The 30–44 age group, which consists of the oldest millennials and youngest Gen Xers, drove the biggest increase in new digital shoppers at the purchase stage, while the 60 and older cohort drove new users at the research stage. Existing e-commerce users also increased their online shopping frequency, including shopping more in familiar categories, as well as across a broader range of products and services.

To better understand how much consumers have shifted towards digital, Euromonitor International analysed results from multiple consumer surveys, fielded from early 2020 to early 2021.

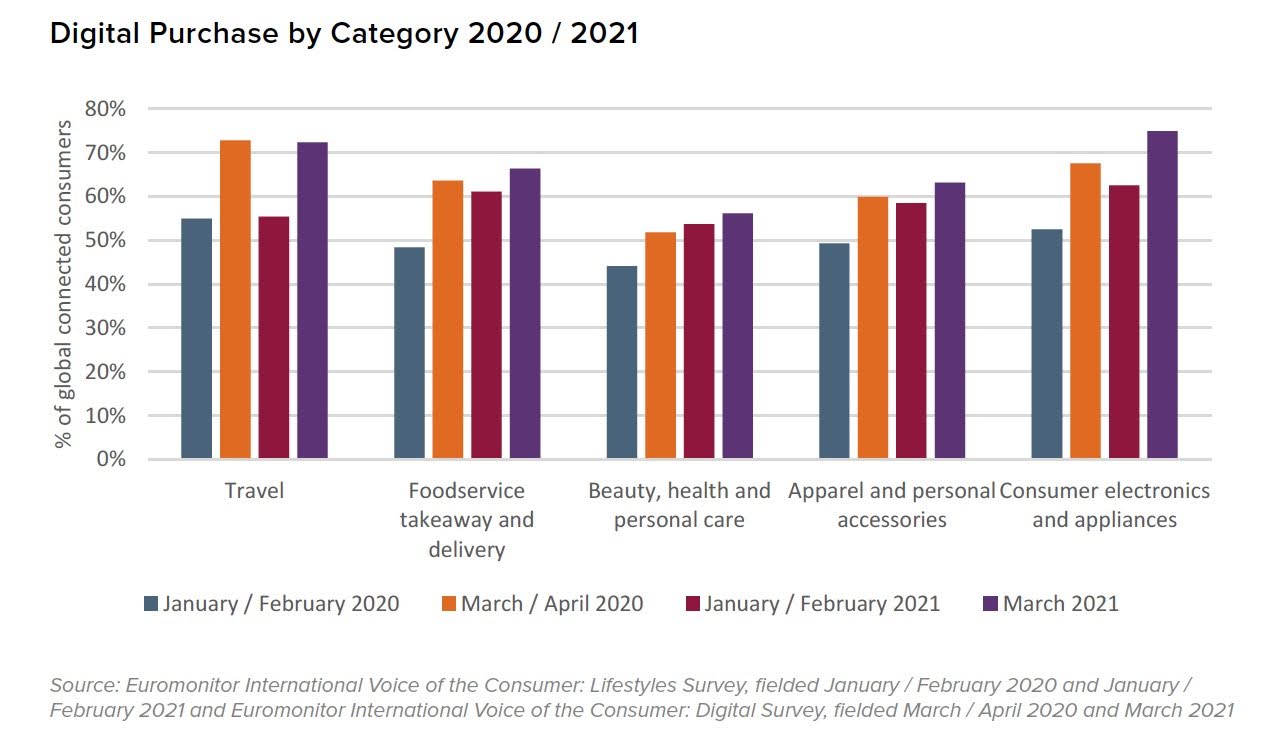

Every industry explored witnessed a jump of 12 to 22 percentage points in terms of connected consumers who said they had made purchases in the digital channel. The crisis led connected consumers to purchase across a broader range of product and service categories. The percentage of minimal online shoppers — connected consumers who did not use digital during the research and purchase steps in the consumer journey or only used digital to shop for one category — dropped significantly from pre-pandemic levels. In turn, there was a sharp rise in the number of heavy online shoppers — those purchasing across four or five of the categories explored in this analysis.

Category Deep Dive

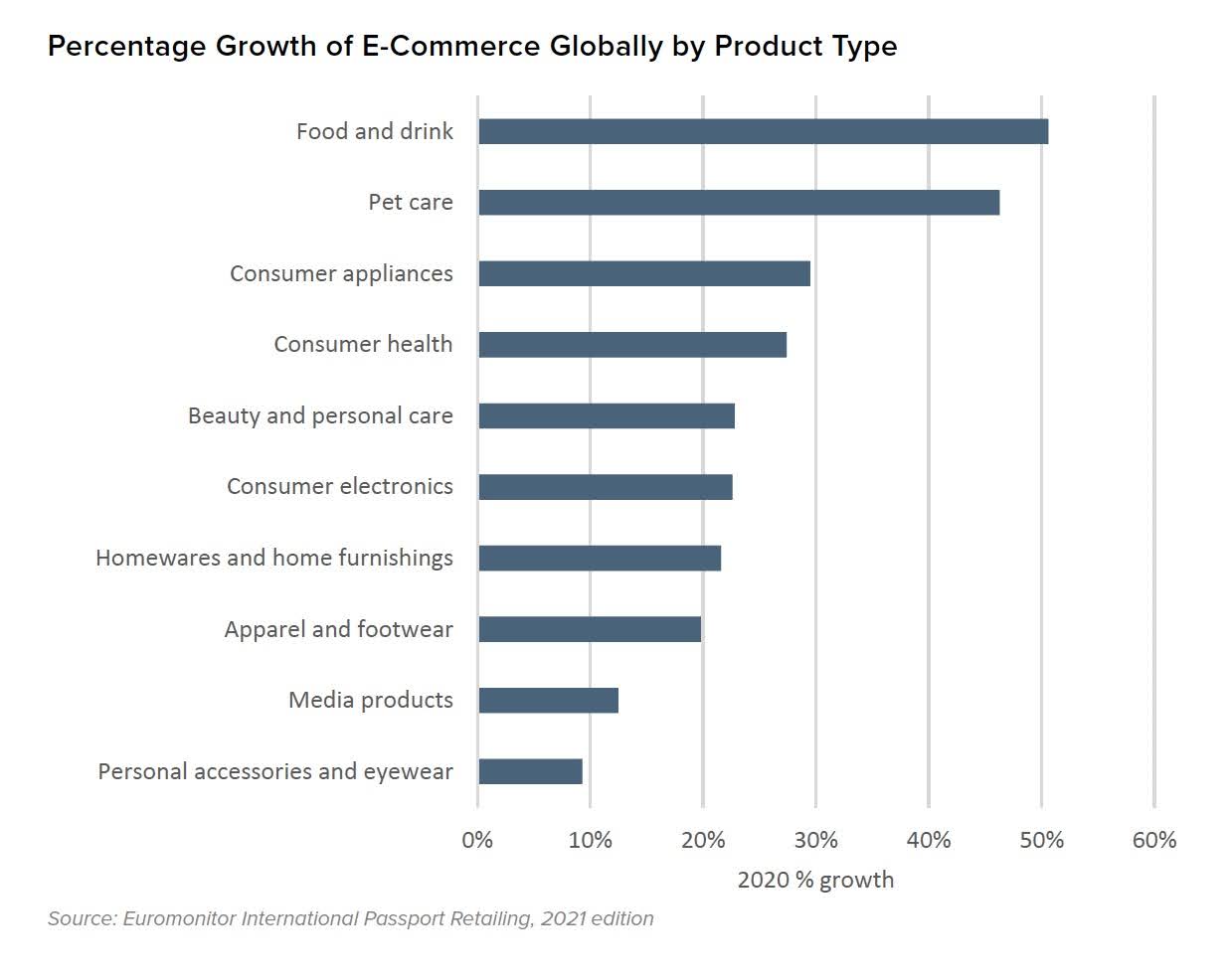

Globally, online grocery saw a significant boost in 2020. To meet this demand, retailers ramped up digital investments and brands launched direct-to-consumer operations. In 2020, food and drink e-commerce expanded by USD84 billion and posted 51% growth — the highest of any product category. The US led this expansion, posting both the greatest absolute value and percentage growth, with a triple-digit rate.

Consumers are likely to return to physical stores more frequently following vaccinations, but Euromonitor International predicts food and drink e-commerce will still expand by 8% in 2021. To survive in this changing competitive landscape, grocery retailers will need to prioritise operational efficiency.

The digital shift will lead to a rise in dark stores, micro-fulfilment centres and automated delivery, as grocers seek to reduce the costs that come with selling more online.

Industry perspective and investment

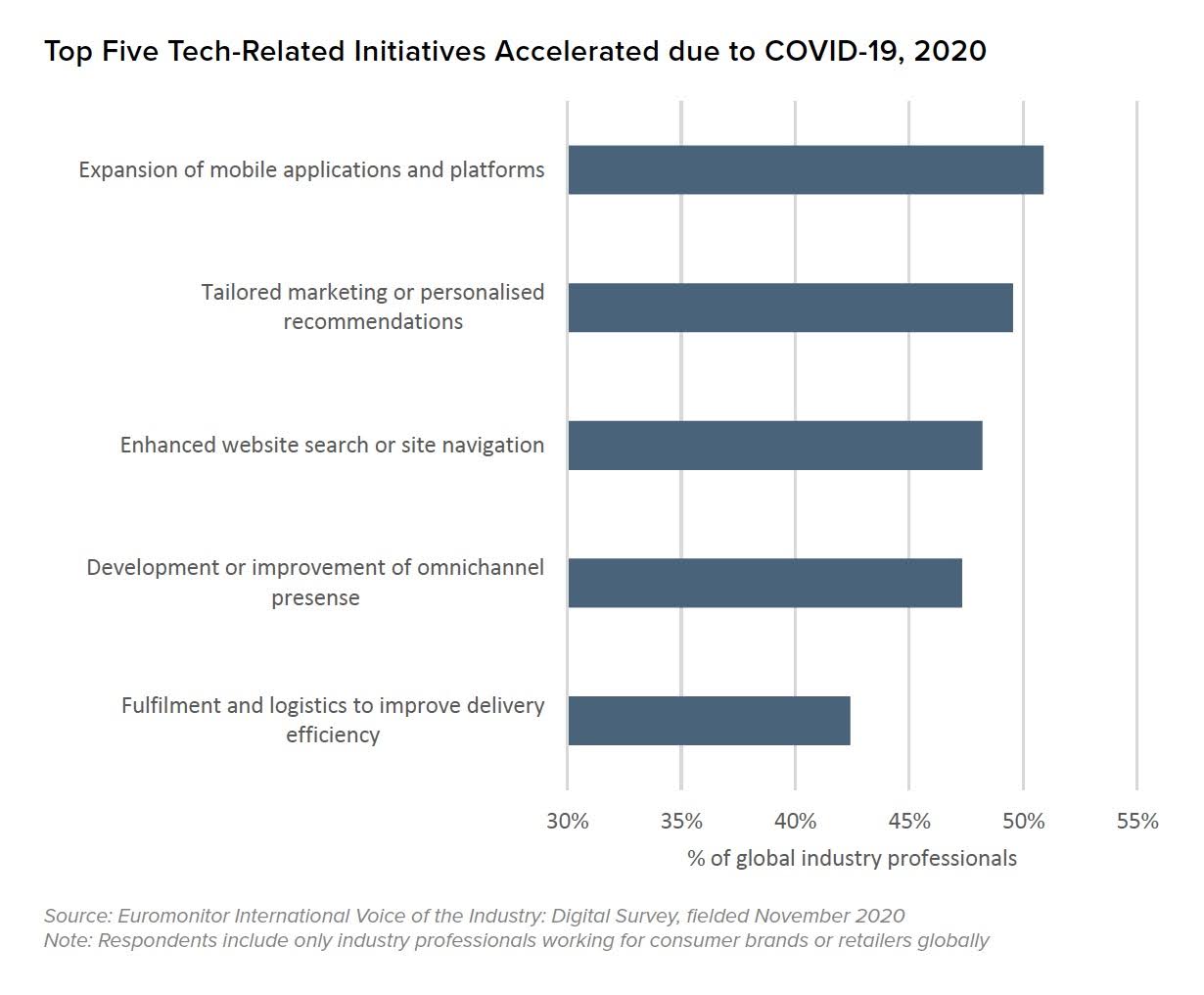

Retailers and brands are more reliant on tech to engage and serve homebound consumers in the online channel. As noted earlier, 73% of retail professionals said their company ramped up their tech-related investments due to COVID-19. Nearly half said they expanded the use of mobile apps and platforms. Other areas included enhanced website search and omnichannel development.

In other questions contained within Voice of the Industry: Digital Survey, retail professionals indicated that most of their investments focused on foundational aspects. In particular, half of retail professionals pointed to it as being the technology that most impacted their business in the past year. They reported using cloud computing most frequently to deploy updates more efficiently and to improve website performance.

Case Studies: Mándameloa Mexico

Two trade associations, Concanaco and Antad, launched Mándameloa, a free online sales platform to help Mexico’s tienditas (small, independent stores) stay afloat. The platform, which enables online payments using WhatsApp, ensures cost- and time-effective order deliveries within a 10-block radius.

Case Studies: Shopify Canada

Shopify, a subscription service that enables companies to launch websites, accept online payments and ship and track orders, benefitted from the surge in small shops going online. This boosted revenue by 86% and profit by 78%, helping the company’s stock become one of the market’s best performers in 2020.

Case Studies: Shopee Singapore

Online marketplace Shopee launched a dedicated platform, Shopee Premium, which allows businesses to customise brand elements and content and gives customers direct access to authentic premium beauty products.

Case Studies: PepsiCo US

A tactic traditionally used by start-up brands, global food and drink giant PepsiCo launched two direct-to-consumer e-commerce platforms featuring its portfolio of products in an effort to reach new consumers.

Outlook

While e-commerce has been the fastest-growing channel for at least the last 15 years, many will look back at this crisis as a key accelerant to the shift. COVID-19 brought many consumers online for the first time and inspired those who were already comfortable shopping online to make more purchases across a broader range of products and services.

Connected consumers also reported visiting stores with less frequency to make purchases. From January 2020 to March 2021, the percentage of consumers saying they shopped in digital channels grew by double digits while physical channels experienced a single-digital drop. Stores will remain an important channel for both discovery and purchase, though the ongoing social distancing measures will reinforce consumers’ comfort with digital platforms and tools.

In-Store Shopping

The role of stores has been changing, with the COVID-19 pandemic only magnifying the need for retailers to rethink how assets are utilised in the future. Although much attention over the last year has been given to the overnight boom in e-commerce and the shift away from stores, physical outlets remain a critical part of the shopping journey. While consumers are migrating towards the online channel, Euromonitor International estimates that 76% of goods will still be bought in store in 2025, though down from 81% in 2020.

Consumer behaviour and motivation

When it comes to purchasing physical goods in stores, connected consumers reported wanting to see or try on something as the primary motivation for making the trip to a retailer.

This is more important for those categories that are more personal in nature, like apparel or beauty, or those that require more consideration, like furniture.

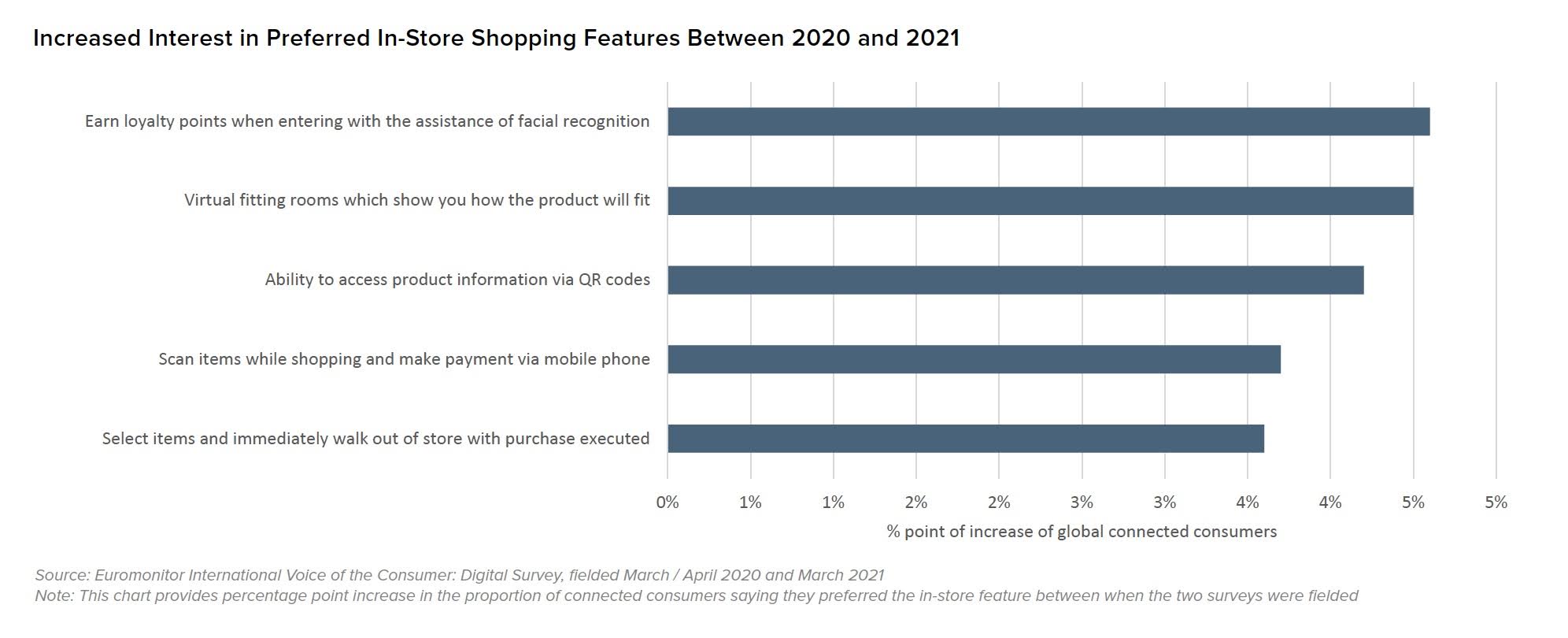

Although not surprising, tech-infused experiences that reduce physical contact saw the greatest bump in consumer sentiment over the last year. More global connected consumers stated technologies like facial recognition, virtual fitting rooms and touchless checkout added more value to their in-store shopping experience than a year ago.

Category Deep Dive

In a year when retail faced unprecedented challenges, grocery stores benefited from the demand for essential items. However, new challenges will arise for grocers in the years ahead, including reduced demand as consumers shift from at-home occasions, rethinking operations to handle order and fulfilment and integrating new technologies at the front-end of the store.

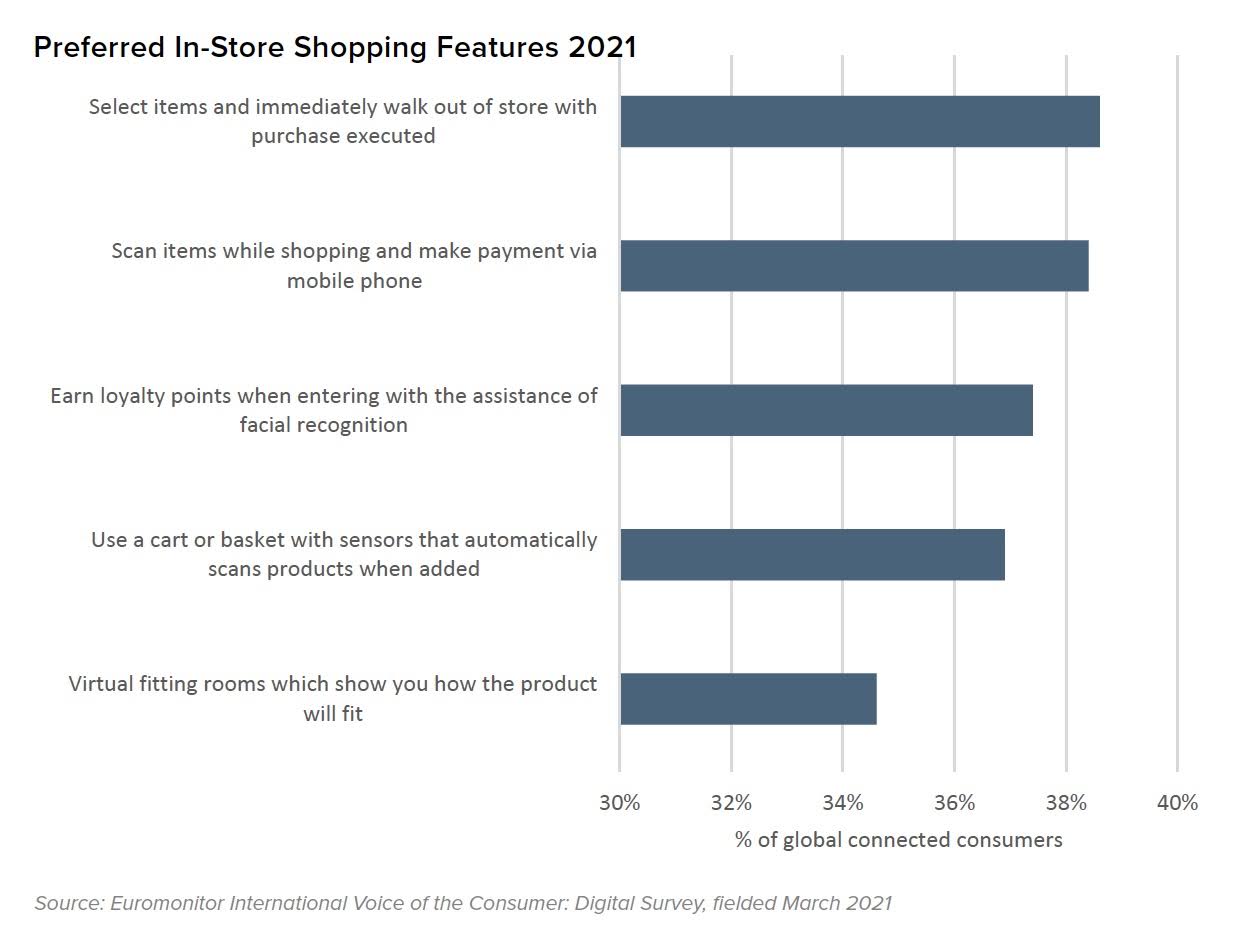

When shopping in physical stores, contactless checkout capabilities were three of the top five features that connected consumers noted would enhance the consumer experience. Almost 40% of connected consumers point to scan-as-you-go, smart carts and walk-in, walk-out technologies as options that would most improve their instore experience.

Retail giants like Amazon, Alibaba and JD.com first pushed the walk-in, walk-out checkout experience, but then technology firms like Grabango and TrivoVision made them more accessible for smaller retailers. This concept got a boost during COVID-19 as contactless retail captured headlines, but its promise of greater consumer convenience and more streamlined operations could continue to fuel checkout-free investments.

Industry perspective and investment

Despite the attention put on e-commerce operations in 2020, 21% of global retail professionals believed COVID-19 would also accelerate initiatives to enhance the store experience. There are several technologies that retailers could leverage in the future to enhance in-person shopping, ranging from robotics to virtual reality to 5G networks.

Technology-based immersive experiences are likely to pick up as consumers return to stores with greater frequency. Of global retail professionals surveyed in November 2020, 45% thought AR / VR and more than half expected that 5G would lead to more sophisticated in-person shopping experiences in five years.

- 21% COVID-19 will accelerate initiatives to enhance the store experience

- 45% of AR / VR will power a more enhanced in-person shopping experience in five years

- 55% 5G will lead to more sophisticated outlet experiences in five years

Source: Voice of the Industry: Digital Survey, fielded in November 2020. Note: Includes industry professionals working for consumer brands or retailers

Case Studies: Zara Spain

Spanish fashion brand Zara launched a feature on its app that allows shoppers to check for product availability in store, reserve a fitting room and purchase items for pick up. The app’s “store mode” function also offers an interactive map guiding customers to the precise location of specific products in store.

Case Studies: Shiseido Japan

Beauty and personal care multinational Shiseido opened its first flagship store in Ginza, Tokyo, offering visitors a touchless shopping experience by using a mobile app to get beauty consultations and testers as well as try-on items virtually.

Case Studies: Burberry UK

In partnership with Chinese tech giant Tencent, Burberry opened its first social retail store in Shenzhen, China designed for customers to interact with products in person or on social media. The luxury fashion house created content for shoppers to unlock via WeChat, including store tours and product information.

Case Studies: Arc’teryx Equipment Canada

Arc’teryx Equipment, a high-performance apparel company, opened its first flagship store in Shanghai, China, which leverages technology to create a more immersive shopping experience. The store features four different experiential huts, such as a “rain room”, which allow customers to try on and water-test the technical functions of its products.

Outlook

Stores will play a critical role in the future of retail, but these physical assets are in the middle of generational change. The continued rise in e-commerce will call into question the fundamental purpose of a channel, challenging retailers to rethink the role of the store for the digital era.

Stores will likely remain a point of discovery for products that require more consideration, whereas retailers that sell a lot of fast-moving consumer goods will need to consider the role this physical space will play in fulfiling e-commerce orders. Technology will play a key role in the execution of this reimagined in-store shopping experience.

Payments

The crisis spurred interest in digital payments, prompting some retailers to go further in contactless options, including card and mobile-based payments, to reduce virus transmission. Digital payments also made inroads online due to growth in e-commerce transactions. In fact, 41% of retail professionals surveyed said that COVID-19 led to the launch or expansion of digital payment options to help facilitate both in-store and online transactions.

Consumer behaviour and motivation

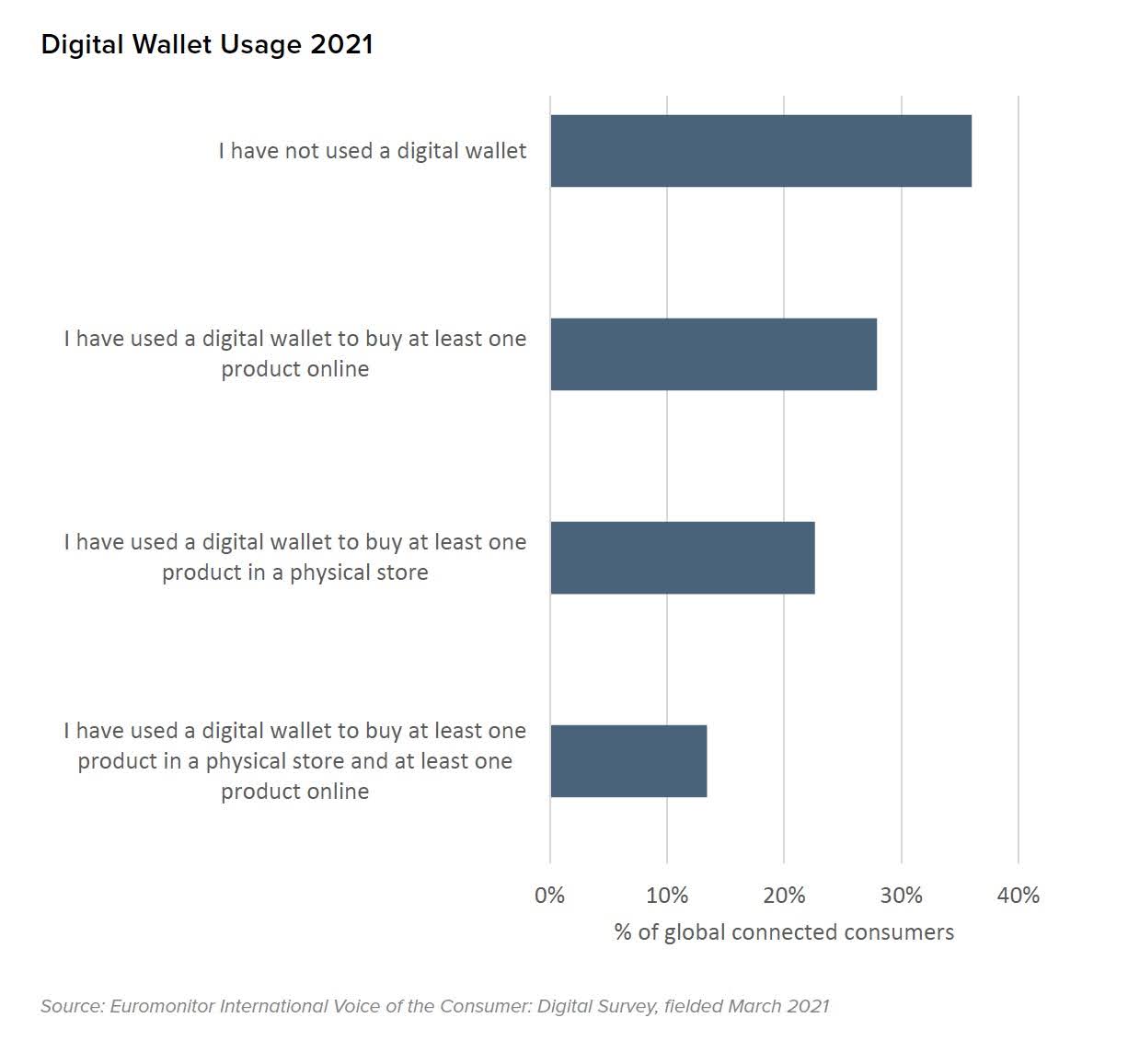

Digital wallets, used both online and in store settings, play a big role in driving digital payments forward.

Providers often cite convenience as a key unique selling proposition (USP) for digital wallets across both settings. According to Voice of the Consumer: Digital Survey, ease of use is the top reason why consumers opt for digital wallets. This sentiment is stronger in emerging markets, where digital wallets do not face as much competition from more established payment methods.

Despite more consumers using digital wallets in 2020, there is still potential for further growth. More than one third of connected consumers globally have still not used a digital wallet, which was defined for respondents as a platform that securely stores users’ payment information and relevant personal details to enable quick purchases. Of those who reported using digital wallets in the last 12 months, usage was most popular online as opposed to in physical stores.

While the cited numbers remain largely unchanged from the 2020 fielding, there is a trend of older consumers adopting proximity digital payments. Consumers in some countries reported using a digital wallet less in store than they did a year ago, which likely reflects the reduction in time spent in physical stores rather than a new aversion to digital wallets. Increased usage, especially among consumers 45 and older, suggests the consumer base may have widened during the pandemic.

Consumer Spotlight

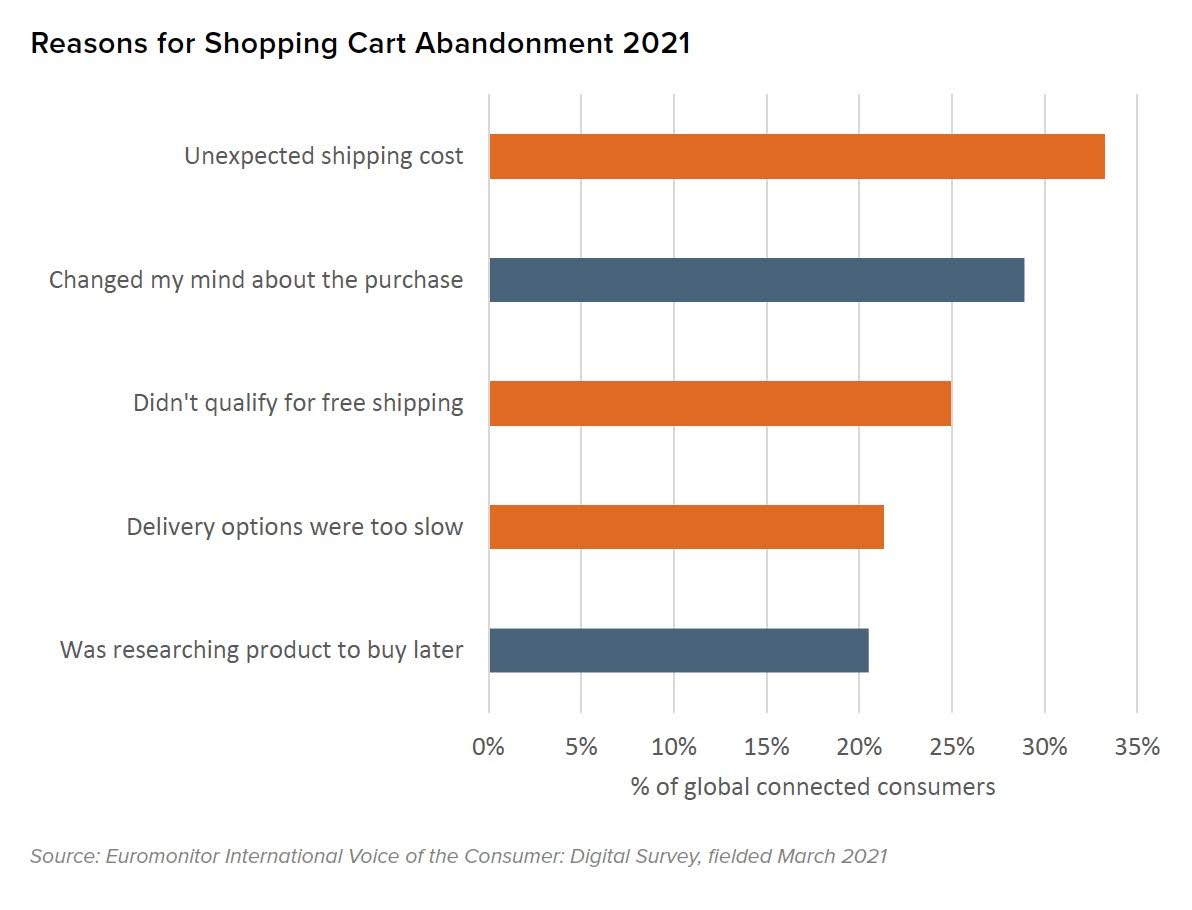

When it comes to e-commerce, one issue that digital wallets help retailers overcome is shopping cart abandonment. Based on results from Voice of the Consumer: Digital Survey, 75% of connected consumers have abandoned a purchase. About 44% say it is for paymentrelated reasons, whereas 51% say it is due to hurdles related to delivery.

When examining the top 15 reasons connected consumers give for abandoning a purchase, consumers were more likely to abort the purchase for delivery reasons rather than payment. The top three delivery-related reasons were all ranked as greater hurdles for executing online purchases compared to those that related more directly to payments.

Unexpected shipping cost was the top reason for shopping cart abandonment, at 33%. The fact that consumers point to delivery concerns over payments may suggest that retailers are already meeting the demands for a seamless checkout experience. However, the general increase in online purchases will continue to ensure that point of sale does not present a pain point on the path to purchase.

Industry perspective and investment

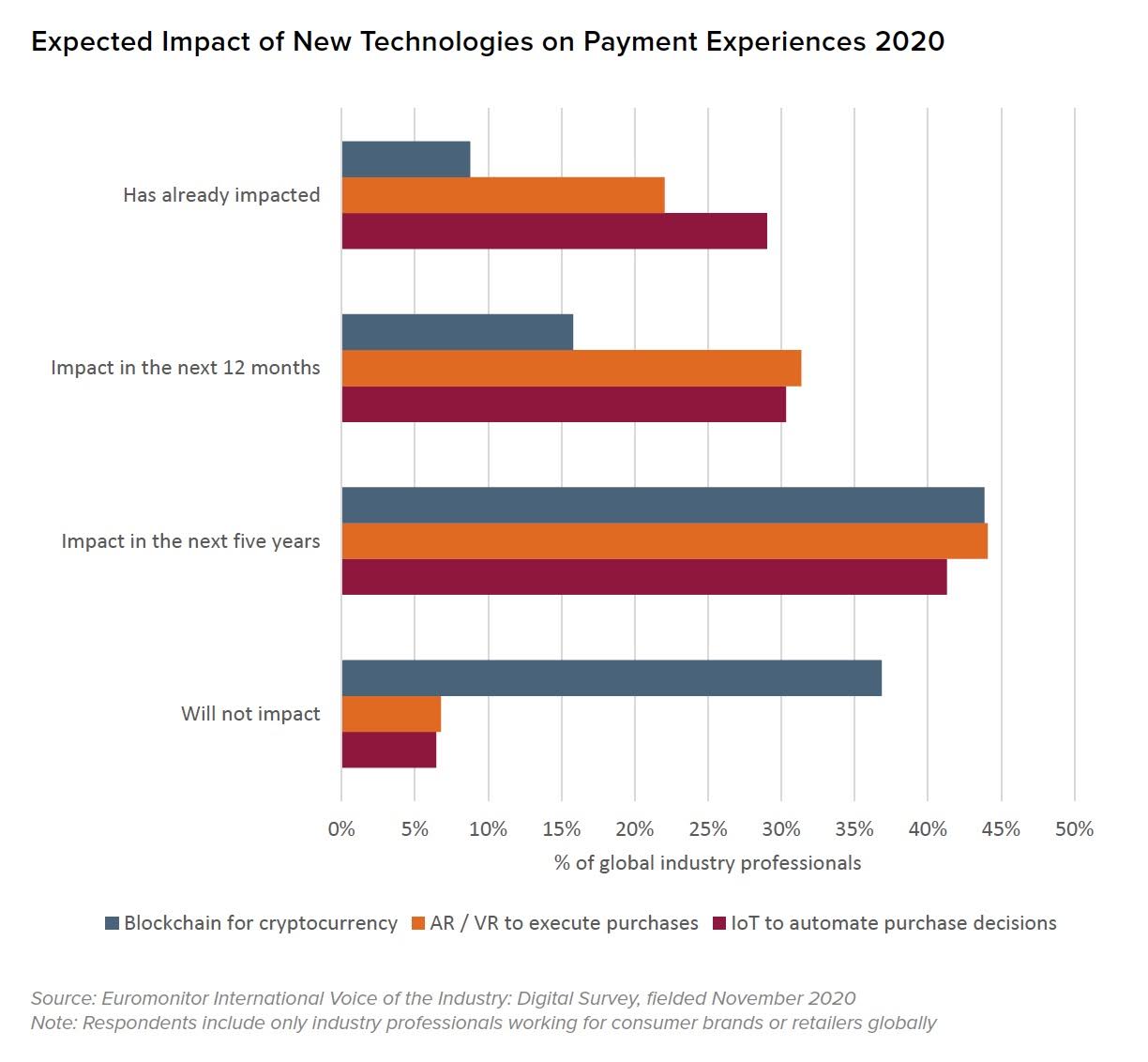

Global retail professionals will continue development of digital wallets, contactless checkouts and new products like instalments. Beyond that, other payment trends will continue to emerge including using blockchain for cryptocurrency, AR / VR to execute purchases and the Internet of Things (IoT) to automate purchases.

All of these technologies are expected to have a greater impact on commerce five years from now. Almost 30% of retail respondents believe that IoT to automate purchases has already had an impact. Overall, they are less confident about a future where blockchain powers cryptocurrency; 37% expect it will have no impact at all, compared with 7% for AR / VR purchase execution and 6% for IoT automation.

Case Studies: PayEye Poland

Polish start-up PayEye launched the first full payment ecosystem based on iris biometrics, which leverages proprietary POS devices and algorithms to detect biometric patterns. Within six months of launch, PayEye was available across 100 outlets, including cafes, grocery stores and hotels.

Case Studies: Amazon US

E-commerce leader Amazon introduced palm-scanning technology that allows customers to pay, present loyalty cards and enter locations with only their hands at a few of its Amazon Go and Whole Foods stores. The service, Amazon One, uses custom-built algorithms and hardware to create a person’s unique palm signature.

Case Studies: Kroger US

Supermarket giant Kroger is experimenting with a high-tech grocery cart that lets customers scan items as they shop and leave the store without having to wait in a checkout line. Shoppers who elect to use the carts are offered a 5% discount on Kroger-branded items.

Case Studies: X5 Retail Group Russia

Russia’s largest food retailer X5 Retail Group partnered with Visa and Sber to launch a facial-recognition system at self-service checkouts across its supermarkets and convenience stores. The biometrics payment system could expand to 3,000 X5 stores by the end of 2021.

Outlook

Contactless card, mobile payment and digital wallet usage, both in outlets and online, are likely to see a long-term boost in markets that already embraced contactless and in-person mobile payments. Other markets, such as the US, were slower to adopt but are now on the rise.

Voice commerce lost momentum during the crisis, as this form of touchless retail did not eliminate safety concerns in the same way that using contactless payments in store did. However, it will likely see a resurgence as its key value add is convenience, which will again become more important to consumers as acute safety concerns subside.

Delivery and Collection

Rising last-mile delivery costs and environmental concerns are forcing retailers to explore new delivery and collection methods. 51% of global retail professionals viewed delivery as a key trend that impacted their market in 2020. Delivery and logistics have emerged as competitive fronts for retailers and third-party delivery platforms, leading to the expansion of delivery and collection services like buy-online-pick-up-in-store options.

Consumer behaviour and motivation

Consumers have an array of e-commerce options available at their fingertips. Customers can have almost everything delivered to their doorstep, sometimes in an hour. Expectations of speed have increased over time as e-commerce giants, such as Amazon and Alibaba, continue to raise the bar, but cost outweighs speed in terms of delivery features desired by consumers. The most desired delivery feature among connected consumers globally is free delivery at 68% while roughly 30% desired either next-day or same-day delivery.

The pandemic is putting a greater spotlight on last mile delivery, including both delivery and consumer collection options. While delivery still reigns as more popular than collection options, many retailers began offering click-and-collect options as an alternative to offset reduced spend in physical channels.

Consumer electronics and appliances remains the top category for click-and-collect services, with 53% of connected consumers saying they make at least some of their purchases in that manner, and 12% saying they make all purchases that way. Food and beverages saw the strongest growth year-over-year as consumers sought safer ways to obtain necessities like food.

Despite increased investment and consumer usage of click-and-collect options, only 22% of global connected consumers viewed it as an important delivery feature, which is down slightly from a year ago. In the last year, consumer interest in click-and-collect services saw the greatest jump in countries like Sweden, France and India, but declined in places like Australia, Brazil, Russia and Chile. Interest remained flat in the US, but did increase in cities with more than a half million residents, where 19% of connected consumers desired this feature as compared to only 14% in cities or towns of less than a half million.

Consumer Spotlight

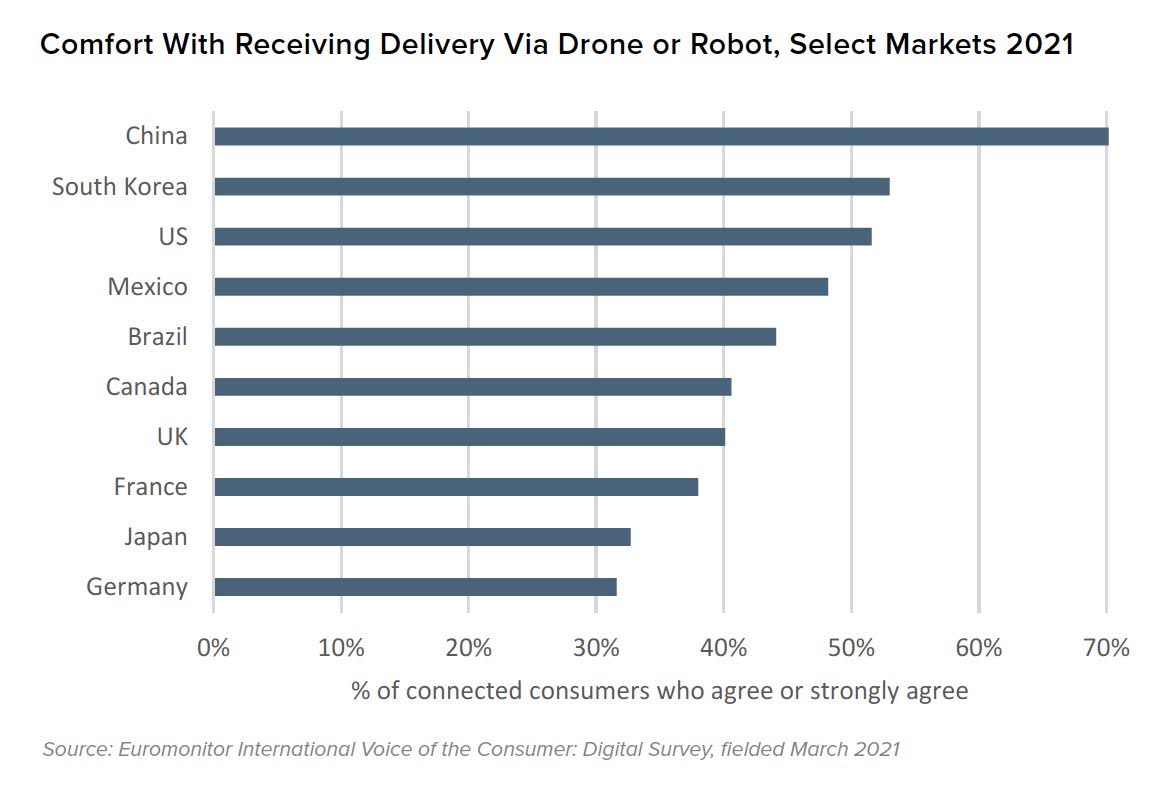

Chinese connected consumers are the most open to new delivery concepts. Based on results from Voice of the Consumer: Digital Survey, 70% of Chinese consumers would be comfortable receiving a delivery via a drone or robot. While this sentiment is strongest among Chinese millennials, there is strong uptake across the population; in fact, less than 5% of the entire Chinese population were against this delivery method. In contrast, only 44% of global connected consumers are open to tech-forward delivery options.

Over the last year, the US saw the greatest leap in comfortability with receiving a delivery via a drone or robot as interest in autonomous delivery rose.

Now more than half of the US population are comfortable with this delivery method, a jump of eight percentage points from the 2020 survey.

The Federal Aviation Administration has been running a pilot program with participants like Amazon, Uber and UPS to advance the framework for commercial drones in the US. In late April, new rules took effect allowing small drones to fly over people and at night, a significant step towards their eventual use for widespread commercial deliveries.

Industry perspective and investment

Many retailers pivoted operations online to better serve digital consumers over the last year. This ranged from expanding last-mile delivery and collection options to infusing the experience with more technology that reimagines how physical assets are deployed. Others acquired or turned to new partners to expand shipping capabilities and made technological investments to speed up fulfilment and delivery options or reduce e-commerce costs.

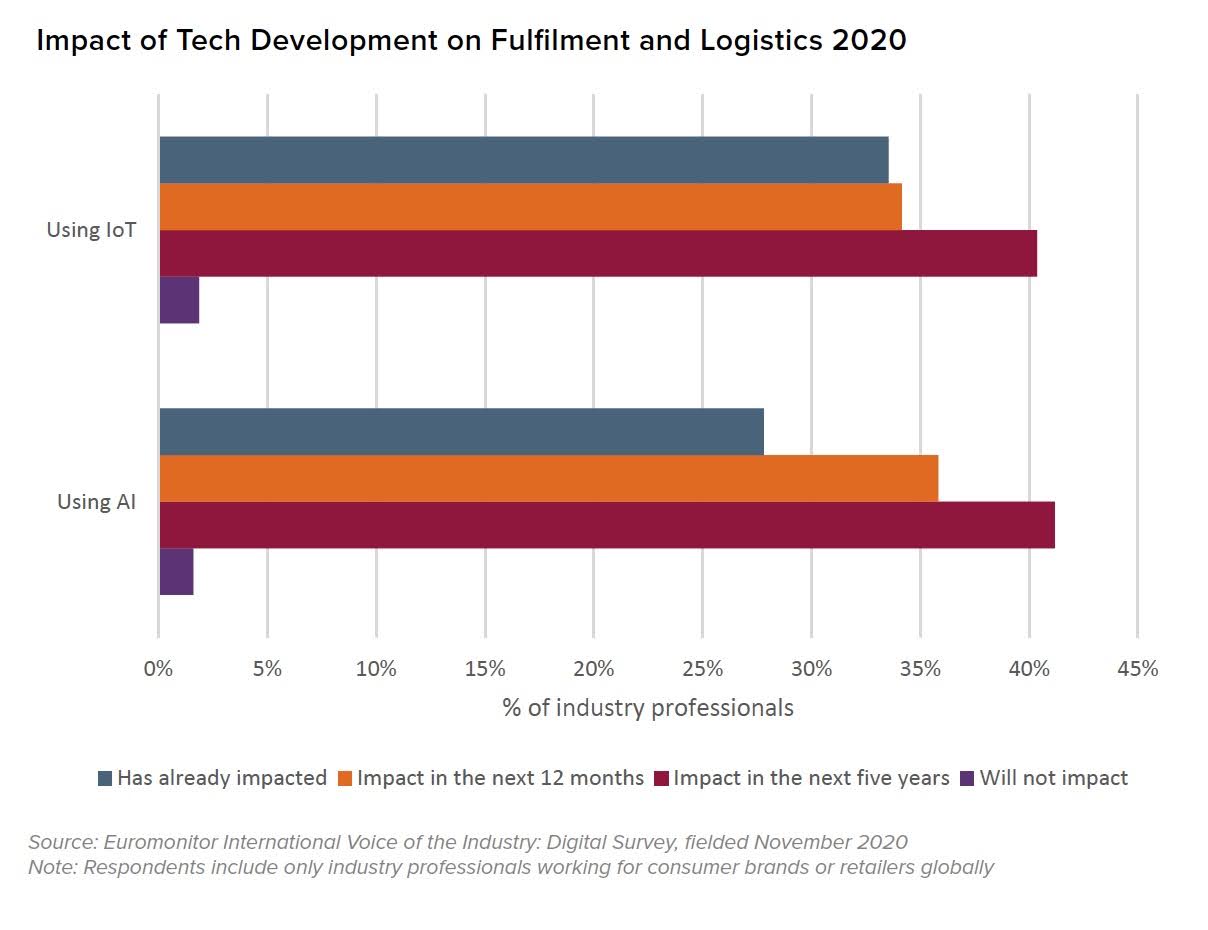

Industry professionals working for consumer brands and retailers view the ability of both artificial intelligence (AI) and IoT to improve fulfilment and logistics as promising.

The somewhat equal split across projected time periods indicates that these initiatives are underway and are expected to gain momentum in the years ahead; however, more than 40% of industry professionals expect IoT and AI will not impact fulfilment and logistics for another five years. The rising importance of e-commerce in retail will reconfigure last-mile operations for years to come.

Case Studies: Walmart US

Walmart acquired JoyRun to add a peer-to-peer product delivery capability and partnered with FedEx to launch an at-home return service. The largest US retailer later announced it began removing its in-store automated parcel tower machines as customers wish to pick up online orders outside.

Case Studies: Weezy UK

Tech startup Weezy piloted its first hyperlocal fulfilment centre in London, offering grocery deliveries in less than 15 minutes. Shoppers can order a range of fresh fruit and vegetables, alcohol, medicine and cleaning products and get quick delivery for just GBP2.95 per order.

Case Studies: Wing US

Since 2019, Wing has completed thousands of on-demand, direct-to-consumer drone deliveries without an accident as part of a pilot in Virginia. In April, the Alphabet subsidiary asked the FAA for approval to consolidate remote pilot operations from local to regional facilities to help it serve additional communities.

Case Studies: Pinduoduo China

Social commerce platform Pinduoduo is popularising the neighborhood group-buying model, which offers buyers relatively low prices while giving sellers more notice of the order. The concept can help reduce inventory, logistics and last-mile costs due to rising e-commerce demand.

Outlook

The reinvention of last-mile delivery and collection is expected to remain an important topic in the year ahead, with 40% of global retail professionals seeing product delivery enhancements as important. Retailers will remain in experimentation mode as they seek solutions to balance the rising interest in e-commerce against rising costs.

Click-and-collect could become mainstay. In North America, curbside pickup has become the dominant click-and-collect mode, given its appeal to suburban and rural settings where vehicles are a necessity. More retailers could follow in the footsteps of foodservice operators by pivoting to a drive-through model to better facilitate in-person collection, even at the expense of reduced foot traffic. Still others will consider their physical assets and the role they can play in getting products closer to consumers before delivery. More retailers will also explore high-tech options, such as robotics and drone delivery, which could be promising in high-density areas to reduce costs.

Conclusion

What to expect going forward

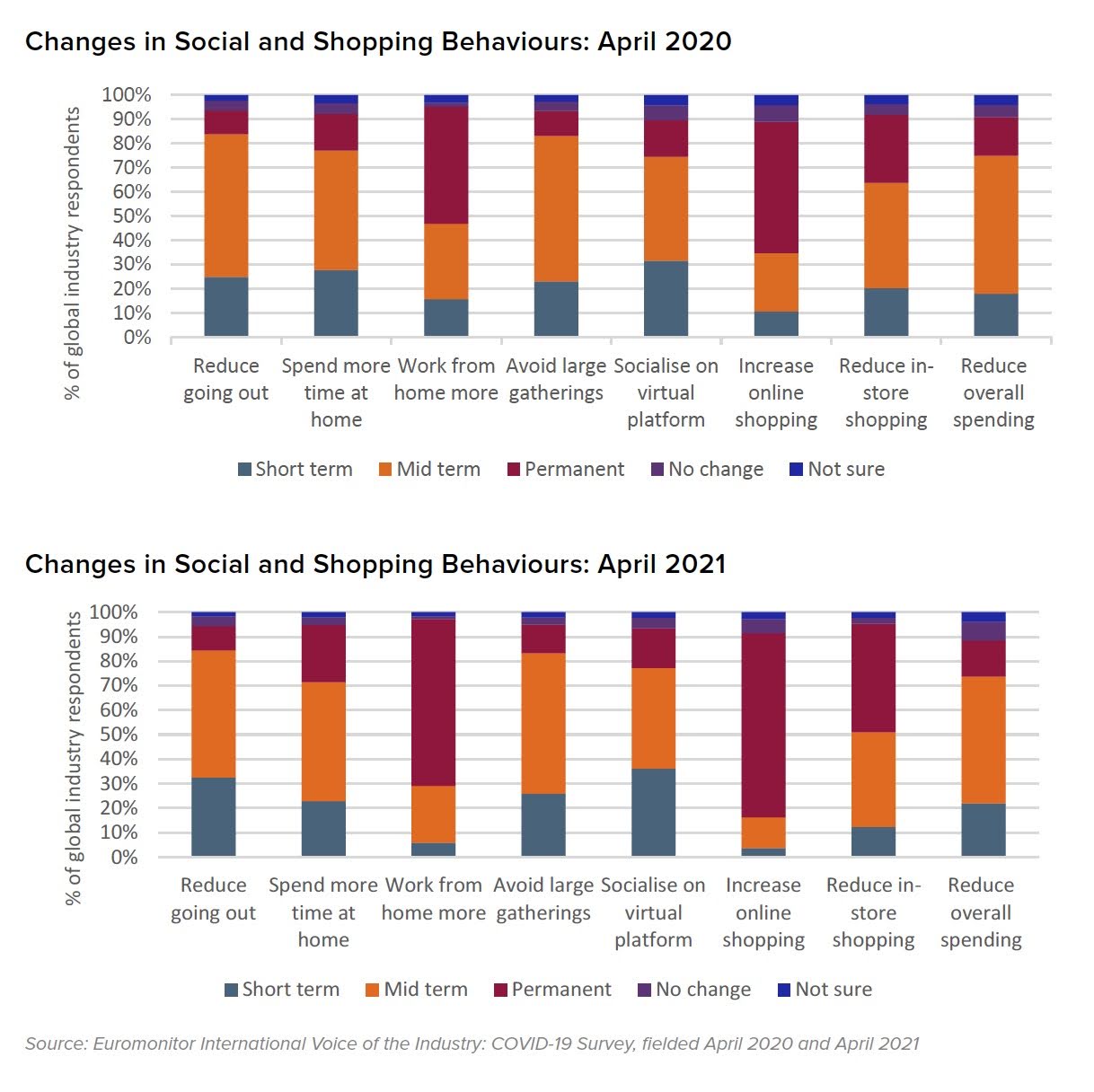

COVID-19 transformed the economic and consumer landscape, ushering in a “new normal” almost overnight. Industry professionals expect this period to have a long-lasting impact to consumers’ social and shopping behaviour. In April 2020, industry professionals surveyed globally were confident that COVID-19 would lead to a permanent shift of consumers shopping online and working from home more; and this confidence has only grown since last year.

The percentage of connected consumers who are comfortable or extremely comfortable with new technologies:

- 42% robots guiding me to specific products within a store

- 27% brands personalising experiences to my mood

- 26% companies automatically reordering products on my behalf

- 20% having a microchip implanted into finger to enable purchase

- 19% companies using DNA to improve recommendations

Source: Euromonitor Voice of the Consumer: Digital Survey, fielded in March 2021

The lasting impact of tech

Consumers have become more comfortable with new technologies, but the level of comfort varies considerably depending upon the action and its perceived intrusiveness. Over 40% of connected consumers are open to having computers involved in the discovery step, but three-quarters are against automatic re-ordering, according to Voice of the Consumer: Digital Survey. Consumers are least comfortable with more intimate experiences, including companies tracking a shopper’s emotions or sharing their DNA in order to receive more tailored products and recommendations.

One of the other profound shifts has been the increased reliance on technology. As noted earlier, 72% of retail professionals surveyed indicated COVID-19 accelerated their company’s digital transformation by at least a year. While technology has been interwoven into commerce experiences in recent years, the growing reliance on technology became that much more apparent during the crisis, as retailers and brands sought to stay connected with consumers.

Where are retailers and brands focusing investments?

Retailers and brand manufacturers have to seriously consider where to invest to remain competitive in the years to come. Results from Voice of the Industry: Digital Survey show considerable activity using cloud and AI. The retail sector is most frequently deploying cloud computing to improve website performance or to better manage supply chains. AI is being used to enhance website search and improve customer engagement. Technologies like AR / VR, blockchain and 5G networks are not expected to gain importance for at least five years when retail professionals expect to prioritise voice-powered applications and supply chain traceability.

Retail Tech Investment

Short term: Actively investing

- 50% Cloud to improve website performance

- 44% AI to enhance website search

- 43% AI to improve customer engagements

- 43% Cloud to manage supply chain systems

- 41% Cloud to create omnichannel experience

Mid term: Expected to ramp up in the next year

- 43% Cloud to showcase user-friendly features on website

- 43% Cloud to deploy updates more efficiently

- 40% Cloud to improve customer insights

- 39% Cloud to innovate faster

- 38% IoT to improve customer engagements

Long term: Likely not to pick up for five years

- 49% Blockchain to improve supply chain traceability

- 44% AR / VR to enhance the path to purchase

- 43% AI for digital testing and product development

- 41% AI and IoT to improve fulfilment and logistics

- 37% AI to handle customer service requests

Source: Euromonitor International Voice of the Industry: Digital Survey, fielded November 2020. Note: Respondents include only industry professionals working for consumer brands or retailers globally

Why should retailers and brands invest now?

Technology will enhance the entire commerce lifecycle from improving operational efficiencies to elevating the consumer experience. Investing in new technologies also positively impacts brand perception.

In Euromonitor International’s Voice of the Consumer: Digital Survey, connected consumers were asked what actions a positive tech-driven experience might trigger and what they would do if they had a negative tech experience. In both cases, consumers reported the tech experience would impact brand perception more than other responses, which included adjusting the frequency with which they visited a store, changing the value of their purchases or how they shared information with others.

The retail industry recognises this shift. Two thirds of retail and brand professionals surveyed expect their digital prowess to be more top-of-mind for shoppers coming out of COVID-19. Going forward, digital will play a foundational role in all retail interactions.

68% of professionals working at retailers and consumer brands expect that consumers will judge them on their digital capabilities post-pandemic. Source: Euromonitor Voice of the Industry: Digital Survey, fielded in November 2020. Note: Includes industry professionals working for consumer brands or retailers